Market Developments

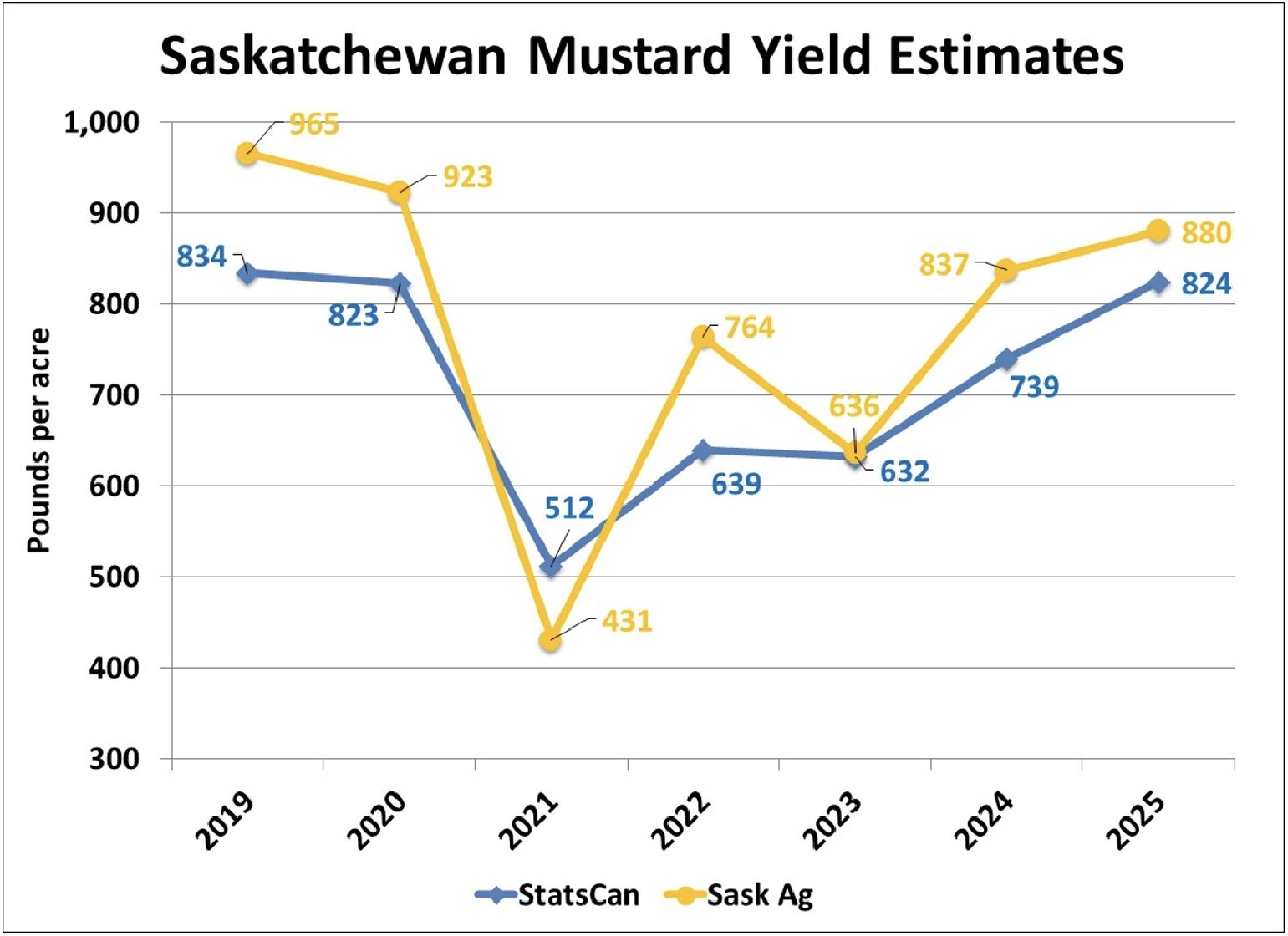

- After two much higher 2025 estimates in earlier crop reports, Sask Ag dropped its mustard yield sharply to 880 pounds (17.3 bushels) per acre. That’s far less than its early October estimate of 1,192 lb/acre. That said, it’s still higher than StatsCan’s Saskatchewan yield of 824 lb/acre. The reason for the reduction is the poor yield in SW Saskatchewan of only 625 pounds (12.5 bushels) per acre. Based on other sources, we think this might be a bit too low but if we adopt it for the province, with StatsCan’s yield for Alberta, the western Canadian crop would work out to 145-150,000 tonnes, 24% less than last year, which limits the increase in 2025/26 supplies.

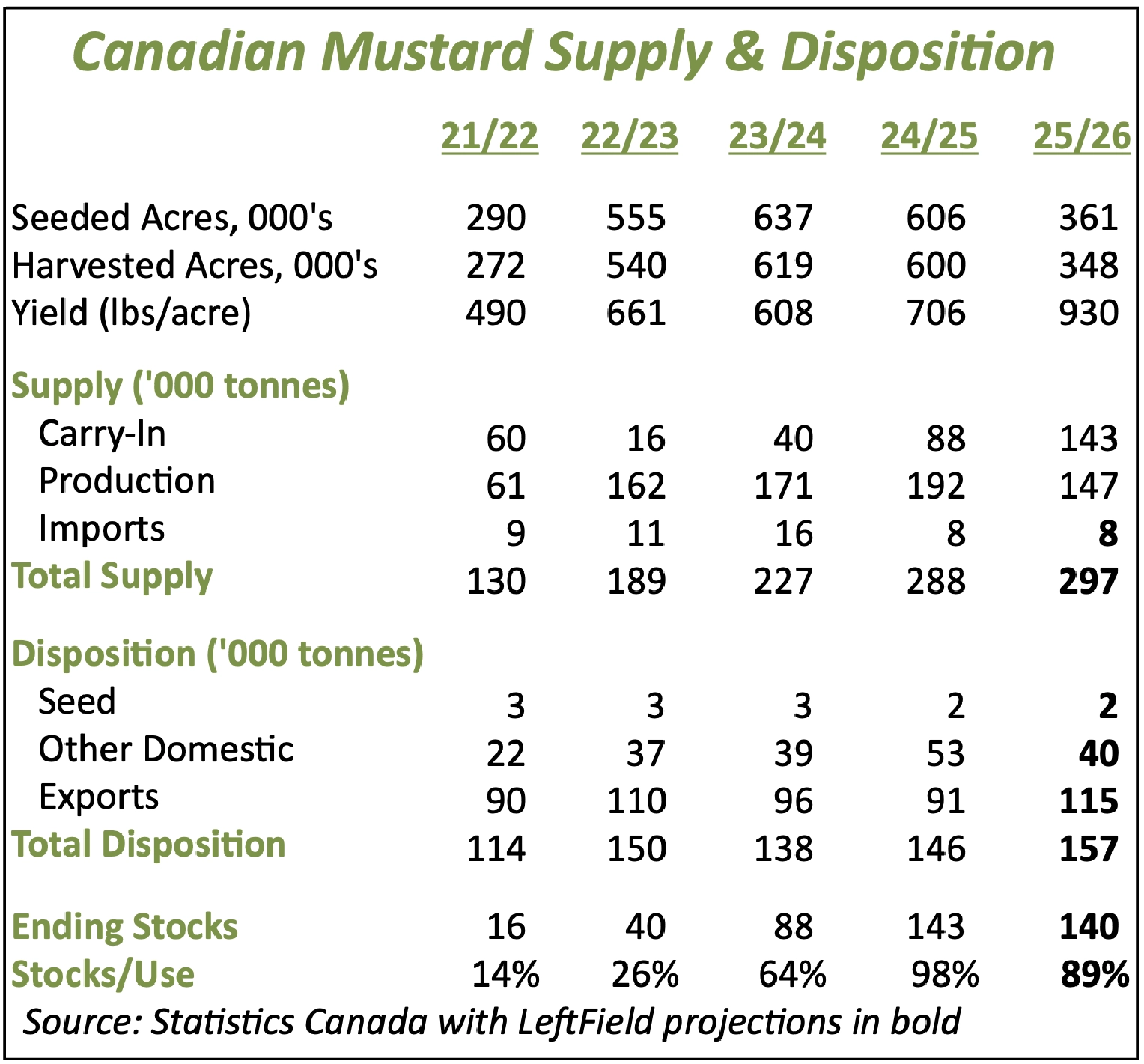

- The Sask Ag crop report also revealed quality issues with the 2025 mustard crop. According to Sask Ag, only 55% of the crop was a 1Can, compared to the 10-year average of 74% while 25% (20%) was a 2Can, 7% (6%) a 3Can and a surprisingly large 13% a 4Can or Sample grade, the most in that bottom category since 2004. Compared to the last three years, when over 160,000 tonnes fell into the top two grades, only 117,000 tonnes would be 1Can or 2Can in 2025/26 (assuming the Sask Ag grades for Alberta production). Keep in mind, some of the old-crop carryover from 2024/25 would also be in the 3Can category.

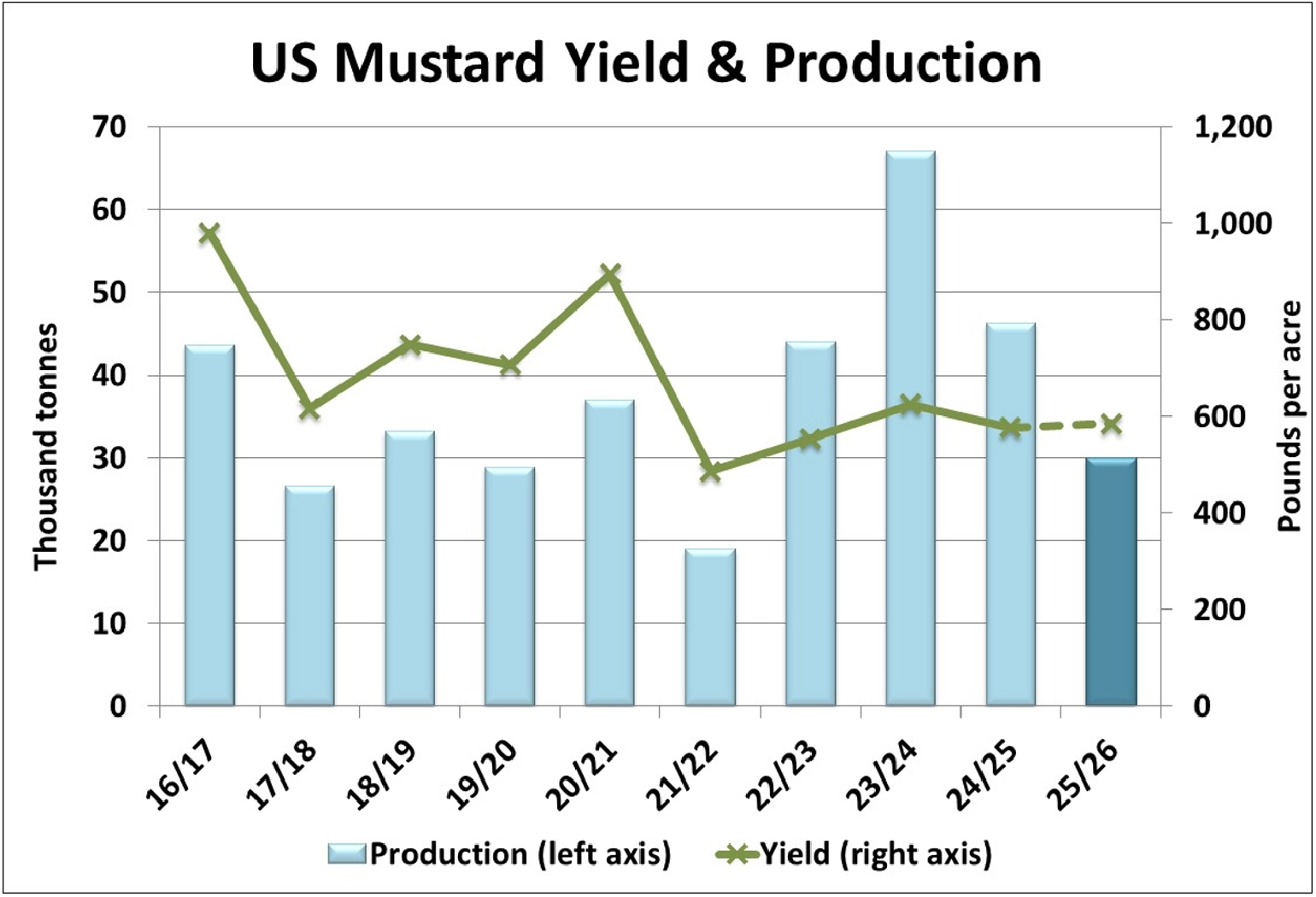

- The USDA won’t release a production estimate for the 2025 mustard crop until next January, but we’re already forecasting a considerably smaller crop. The USDA (NASS) shows seeded area at 165,000 acres while the more accurate FSA acreage declarations are reporting 123,000 acres, down 34% from last year. The yield is still a large question mark but an average yield at 585 lb/acre is a reasonable place to start. The result is a crop of 66 mln pounds or 30,000 tonnes, down 35% from a year ago. To maintain adequate supplies for 2025/26, US imports would need to increase, which we’re pegging at 135 mln pounds or 61,200 tonnes, roughly 7,000 tonnes more than last year and the most since 2022/23. This is providing stronger demand for Canadian yellow mustard.

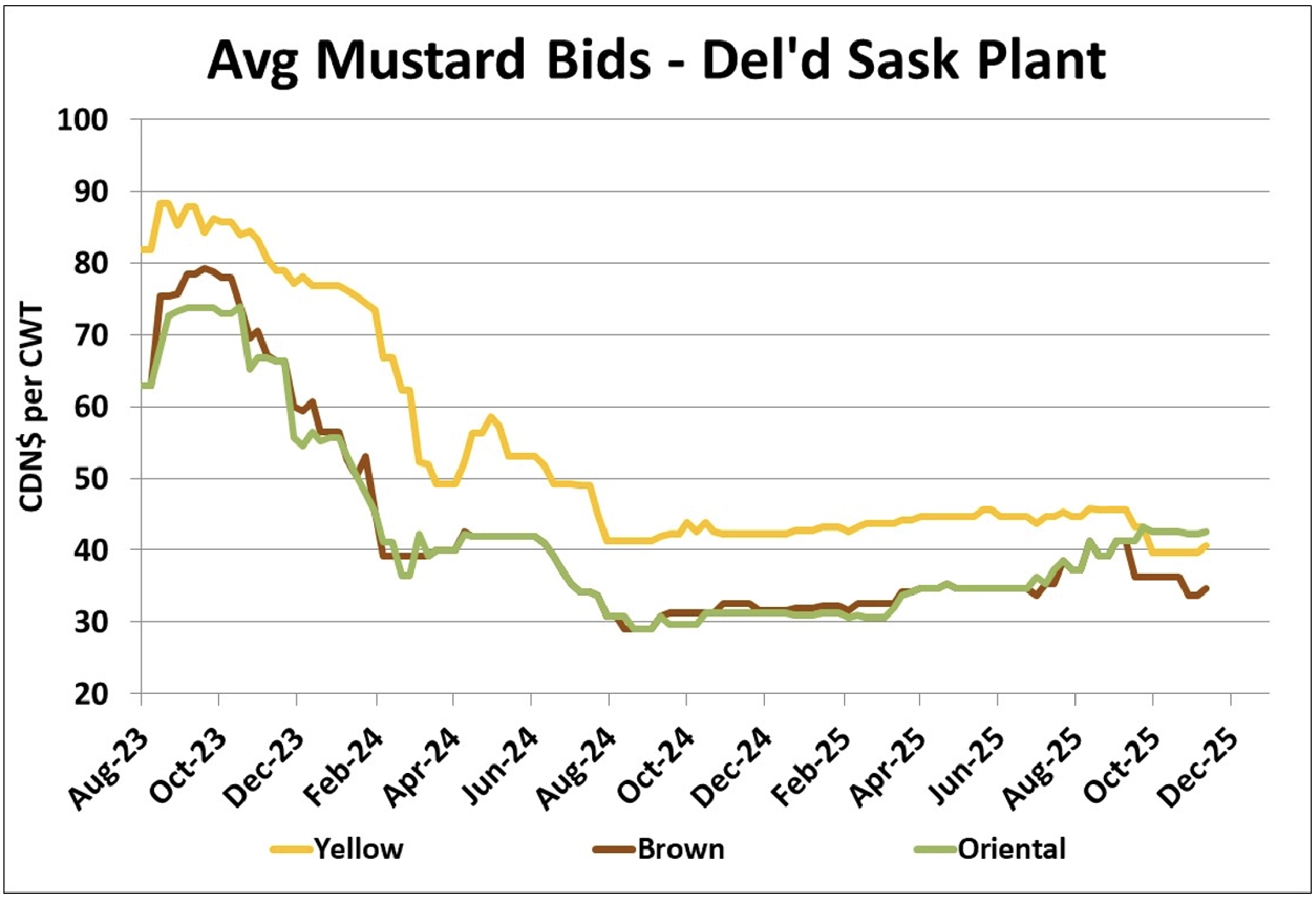

- From a long-term perspective, Canadian mustard bids largely seem to be moving sideways, close to multiyear lows but when viewed over a shorter timeframe, there could be a bit of life entering the market, with some small bounces in yellow and brown mustard bids. It’s still early days though and more confirmation would be needed to indicate a meaningful move is underway.

Outlook

On paper, Canadian mustard supplies still appear quite comfortable, but with two years in a row of quality issues, the amount of mustard available for processing and export isn’t as plentiful. Contracted mustard is able to meet demand for now but some additional mustard will be needed later in the season, which could require more aggressive bidding to convince farmers to open their bins. Oriental mustard moved higher earlier but yellow and brown may have more upside potential later in 2025/26.

{kind=link}

{kind=link}

{kind=link}

{kind=link}