Market Developments

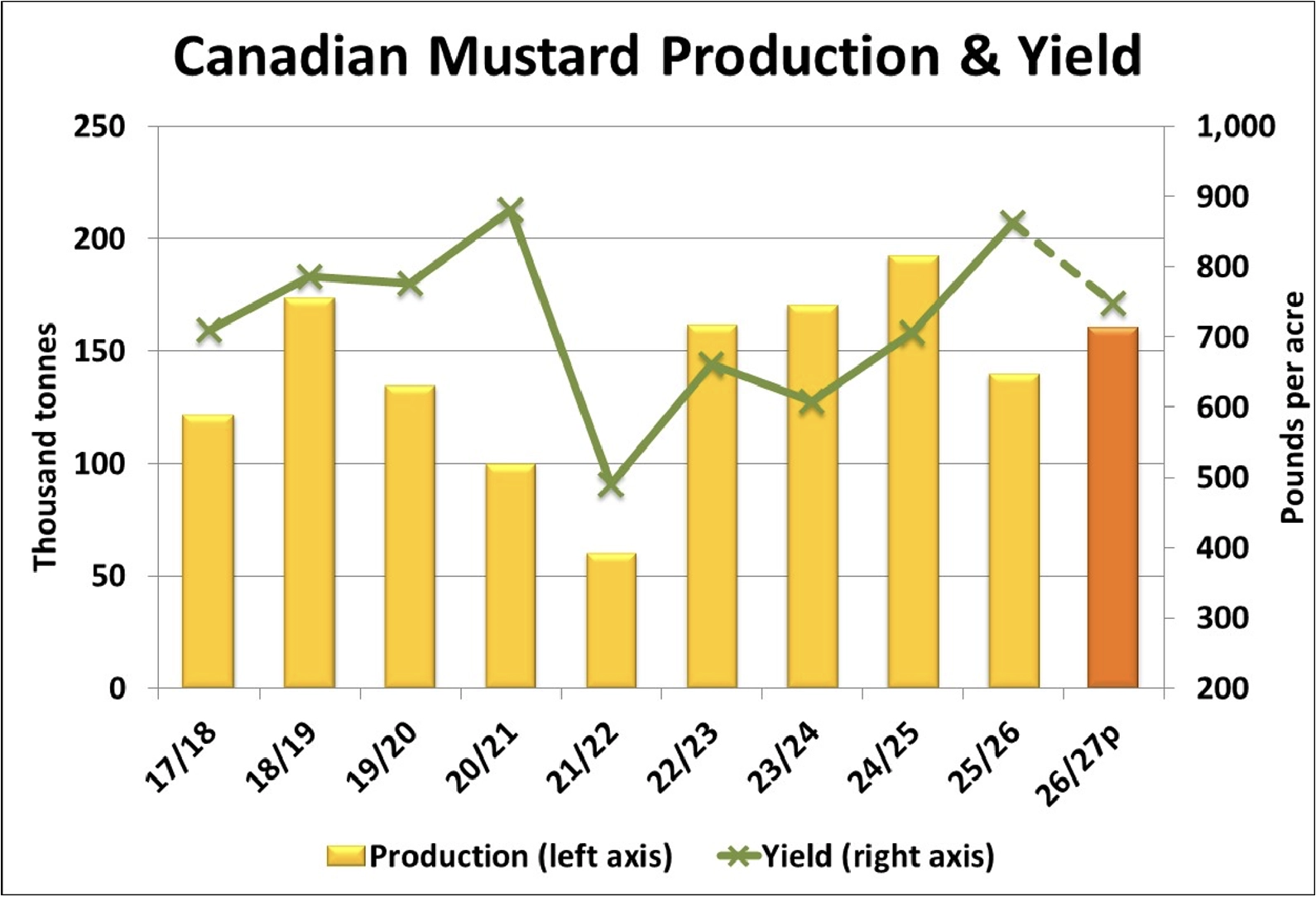

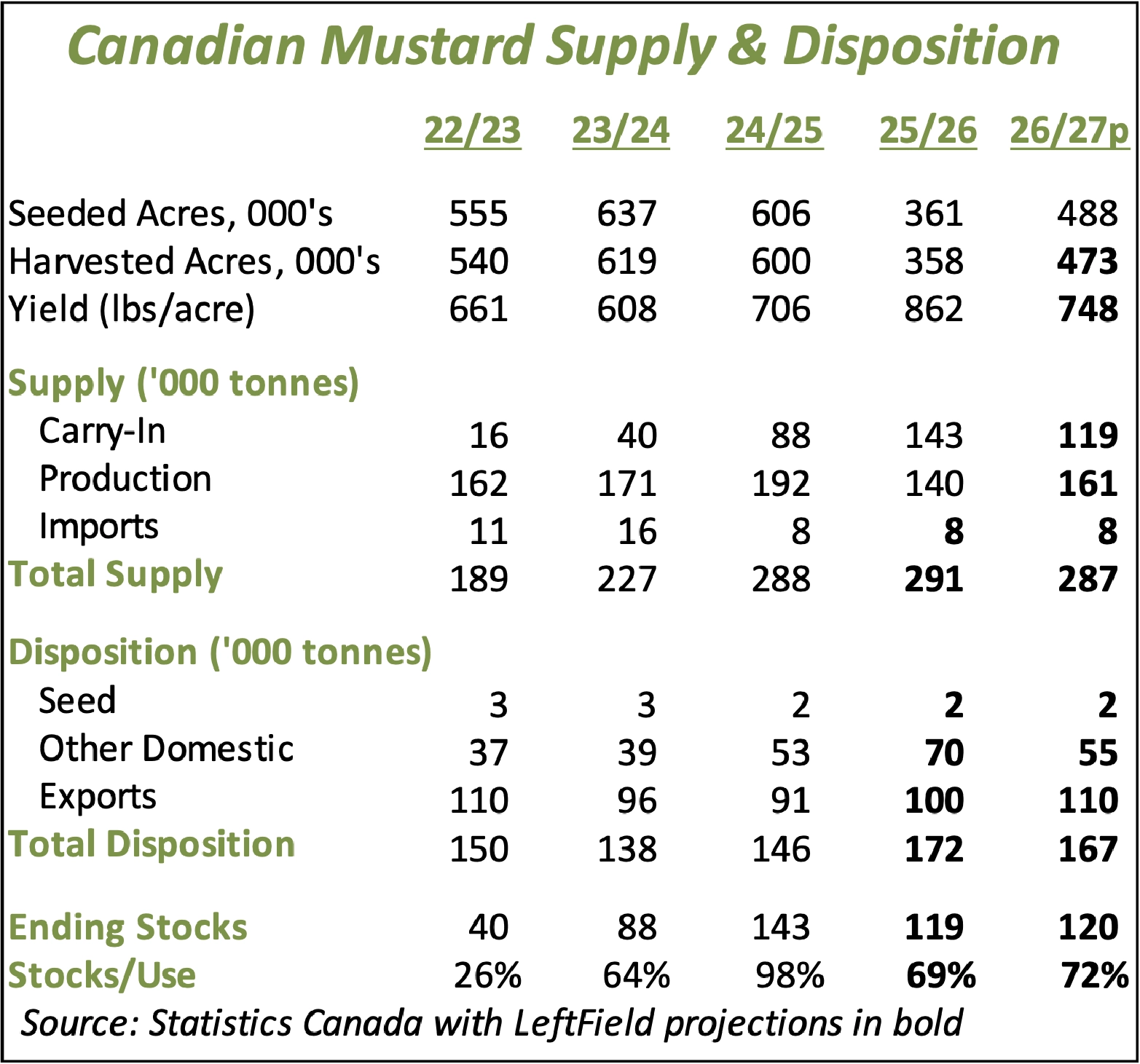

- In the last few years, mustard-growing areas of western Canada have experienced several subpar seasons, which dragged down the average yield. As a result, for our 2026 guesstimate, we’ve shifted to a longer-term olympic average based on 10 years, rather than using just the last five years of mostly low yields. While it’s not a huge difference, going from 658 lb/acre to 748 lb/acre adds 20,000 tonnes to our 2026 mustard production forecast. The 161,000 tonne crop would be 15% larger than last year and even with a smaller carryover, supplies in 2026/27 would be nearly unchanged from the current year.

- When StatsCan issues its March 31 stocks report, we expect to see mustard inventories close to last year’s high level, or even slightly higher. While the 2025 crop was considerably smaller, the carryover from 2024/25 was much bigger, keeping supply levels elevated. Keep in mind, a sizable percentage of those supplies are lower grades, with as much as 40-50,000 tonnes a 3Can or Sample grade. Even so, the supplies of 1Can and 2Can mustard are still well above previous years and will continue to weigh on prices.

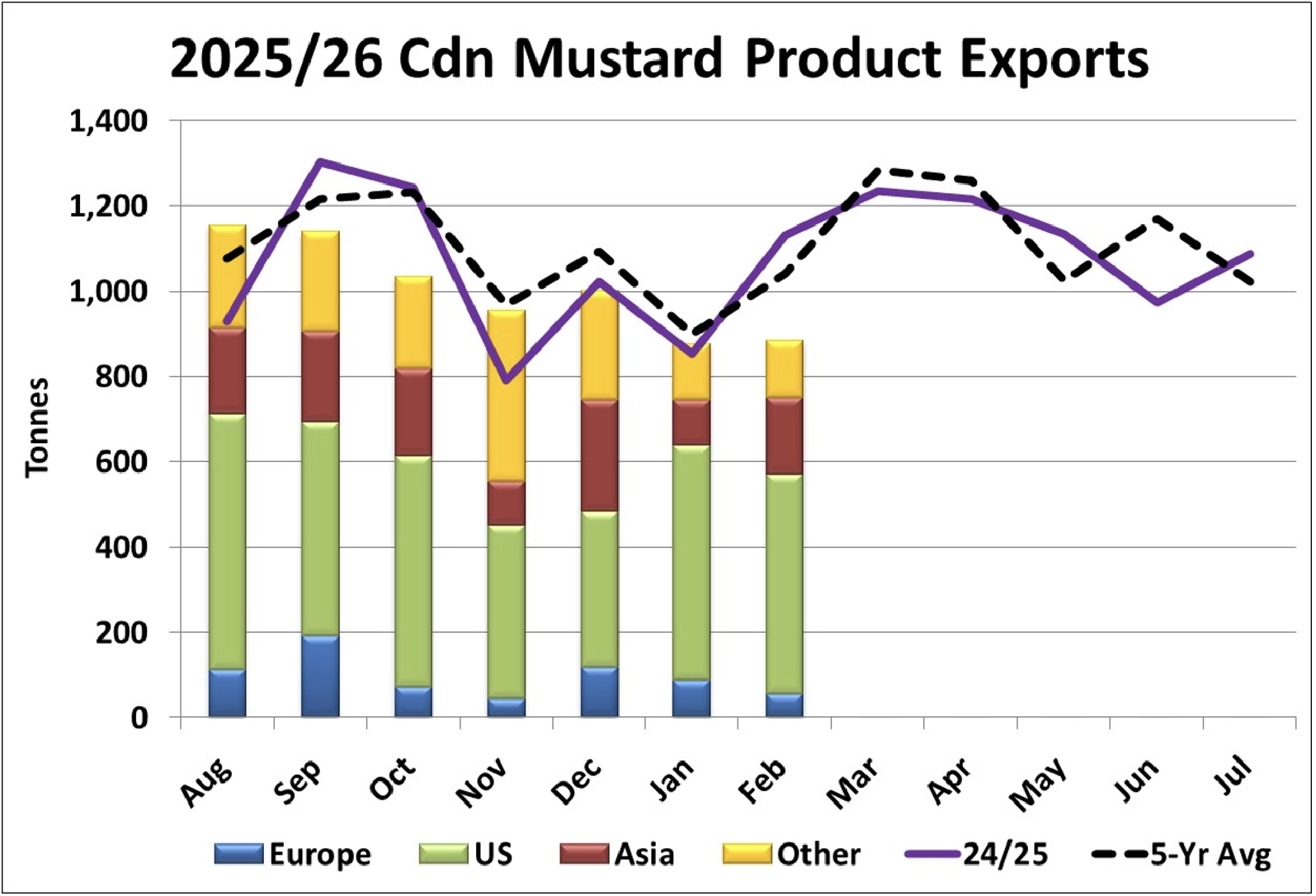

- So far in 2025/26, Canadian exports of mustard products (flour, meal and prepared mustard) have been running a bit below last year and are trailing the average. In February, 883 tonnes were exported, bringing the year-to-date total to 7,050 tonnes versus 7,270 last year and the 5-year average of 7,525 tonnes. While the US is still the dominant destination, those volumes are lagging so far in 2025/26 while exports to most other regions, particularly Asia, Europe and the Middle East are up over last year.

- Similar to Canada, we’re expecting a rebound in US mustard plantings for 2026 at 160,000 acres. With an average yield, production would come in at 86 mln pounds or 39,000 tonnes, up 21% from last year. Even so, that wouldn’t result in heavy supplies and we’re forecasting 2026/27 imports at 51,000 tonnes or 112 mln pounds, 3% more than the current year. Even with a larger 2026 crop and a few more imports, US supplies would expand to only 203 mln pounds, in line with the historical average.

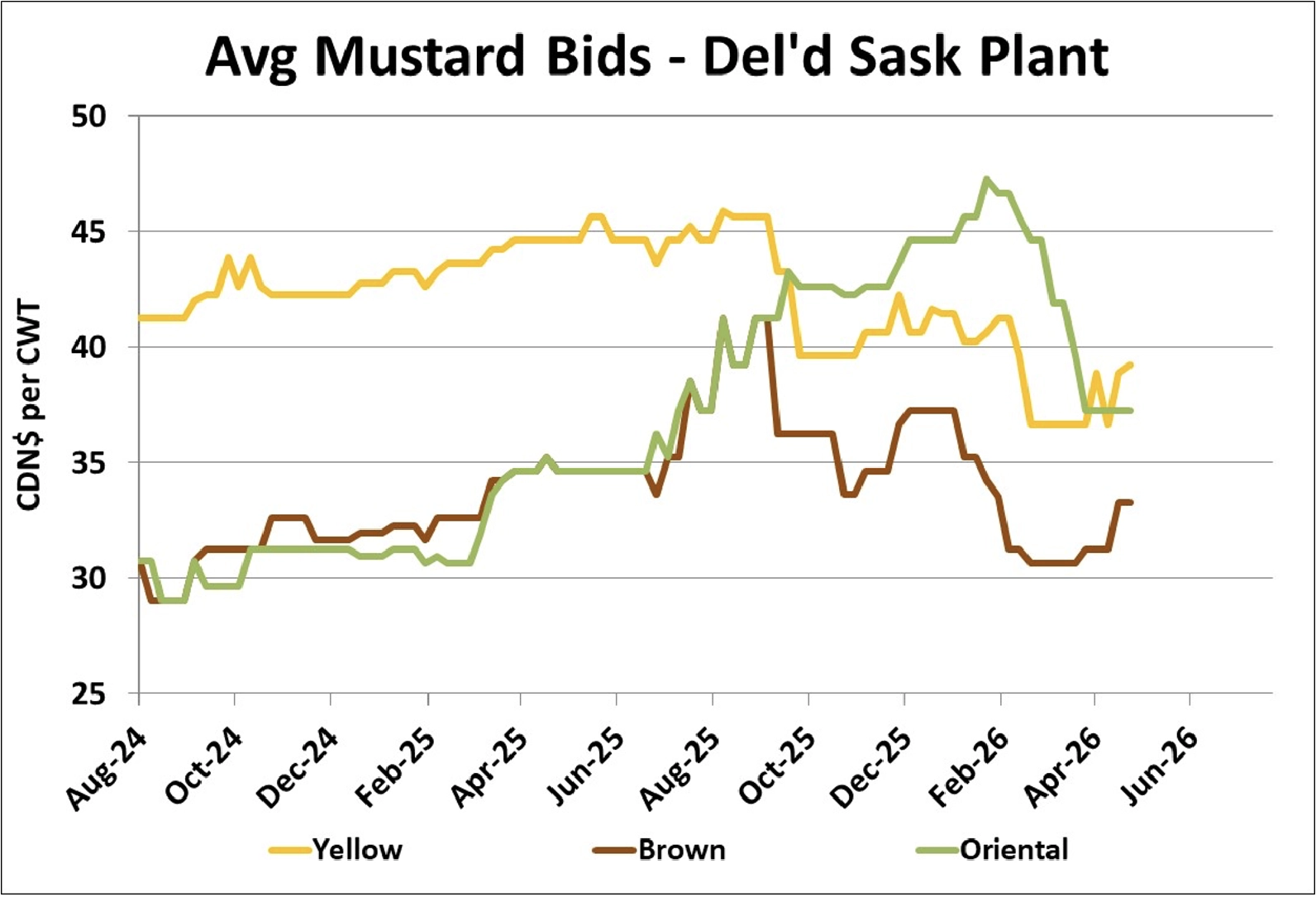

- There’s been some late-season movement in average old-crop mustard bids, with noticeable gains in both yellow and brown mustard. That said, these increases in the average bid likely apply to just one or two buyers and don’t represent a widespread move or large volumes. In fact, most of the feedback in recent weeks has indicated that amounts traded recently are very limited. Meanwhile, oriental mustard bids remain weak. The new-crop indications show a return to more normal price spreads for the three classes, with higher yellow bids to offset the normally lower yields and oriental and brown bids very close together.

Outlook

There have been some late adjustments in some buyers’ mustard bids, but we’re not convinced they reflect a real change in market direction. Most focus is now on the 2026 crop and a rebound in acres sets the stage for another year of comfortable supplies, although yields will still need to cooperate. Our latest outlook suggests overall mustard supplies will be similar next year, although acreage shifts among the types could mean more price strength for brown and less for oriental.

{kind=link}

{kind=link}

{kind=link}

{kind=link}