Market Developments

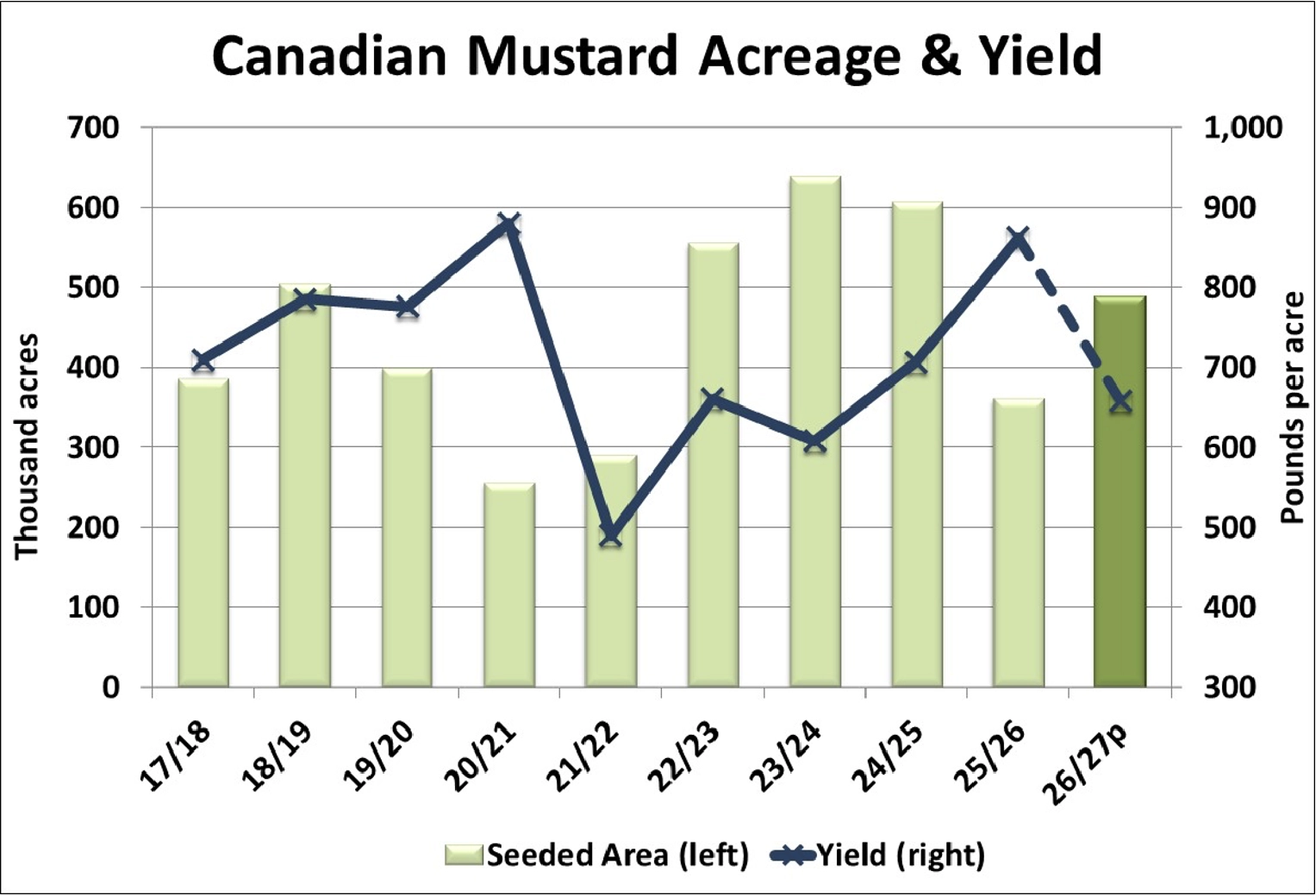

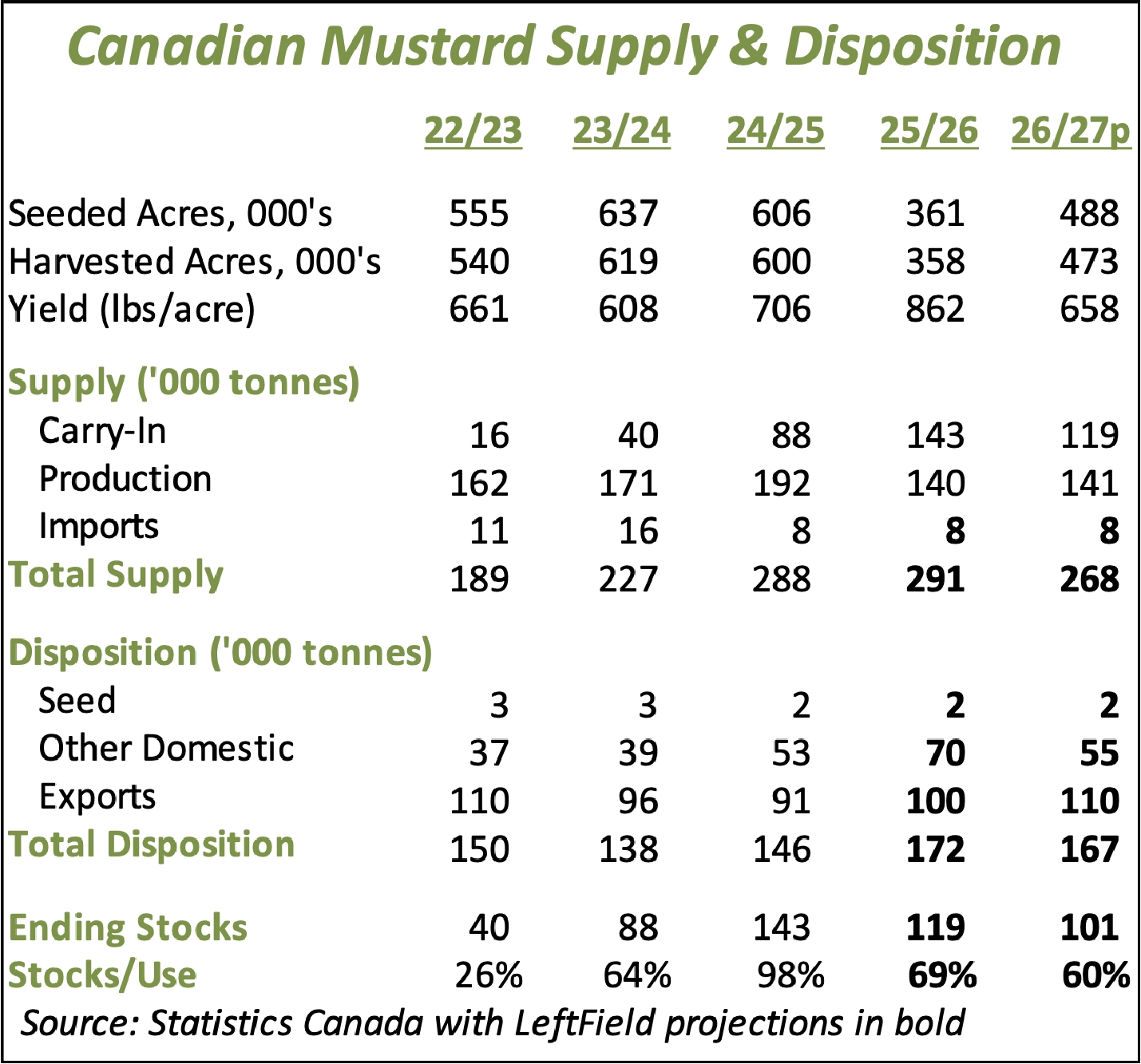

- The StatsCan estimate of 2026 mustard area came in at 488,000 acres, 35% more than last year’s low point and close to our estimate of 500,000 acres. StatsCan doesn’t issue a breakdown by type at this point, but price signals suggest the largest percentage increase would be for oriental mustard, with our guesstimate at 130,000 acres (up 69%), followed by yellow at 260-265,000 acres (up 30%), with 95,000 acres of brown mustard (16% more than last year).

- Despite the large acreage increase, a drop in the overall mustard yield back to the olympic average of 658 lb/acre (862 last year) would mean the 2026/27 crop would end up at 141,000 tonnes, nearly unchanged from last year. A drop in old-crop carryover however, would mean lower supplies in 2026/27.

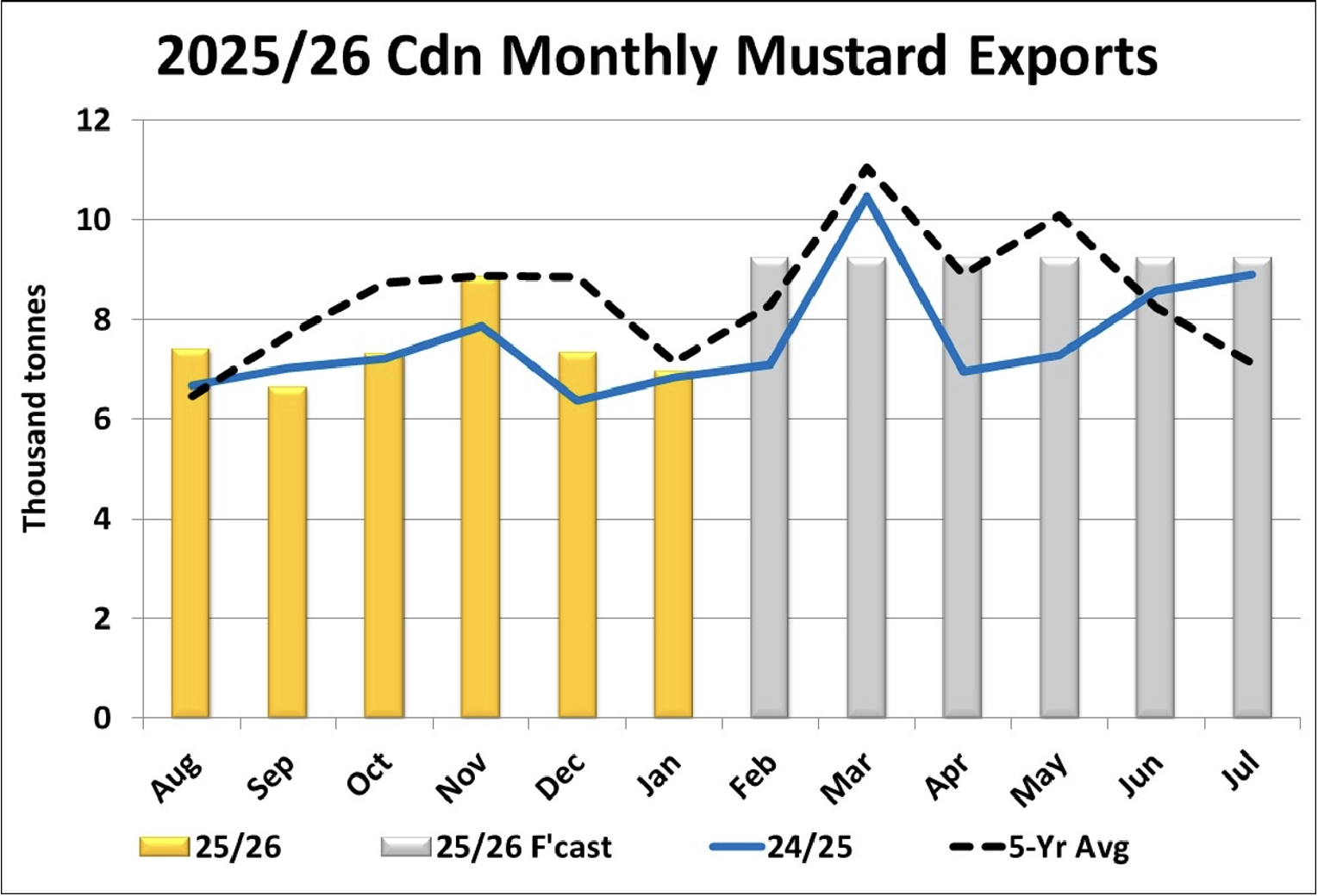

- Canadian mustard exports were disappointing again in January at just under 7,000 tonnes, marginally higher than last year but a bit below the 5-year average of 7,100 tonnes. Through the first half of 2025/26, exports are 44,600 tonnes, still ahead of the last two years but trailing the 5-year average of 47,700 tonnes. Exports to Europe are ahead of last year while volumes to the US are trailing. We’ve been concerned about mustard exports for a while and have now trimmed our full-year export forecast by 10,000 tonnes, now at 100,000 tonnes, still the highest since 2022/23. Exports tend to improve in the second half of the marketing year, and monthly volumes would need to average 9,200 tonnes for the final six months.

- The amounts aren’t large, but the change in Kazakh mustard exports from previous years is noticeable and raises a few questions. Through the first four months of 2025/26, Kazakhstan reported 6,400 tonnes of mustard exports, the strongest pace since 2018/19. The main destinations for these exports are in western Europe. It’s worth noting that Kazakh mustard production declined slightly to 17,100 tonnes in 2025/26 and was far below the 2018/19 high of 45,700 tonnes. We don’t have a way to nail down the origin of the Kazakh mustard but suspect some of it could be coming from Russia to bypass the EU’s 50% tariff on Russian mustard.

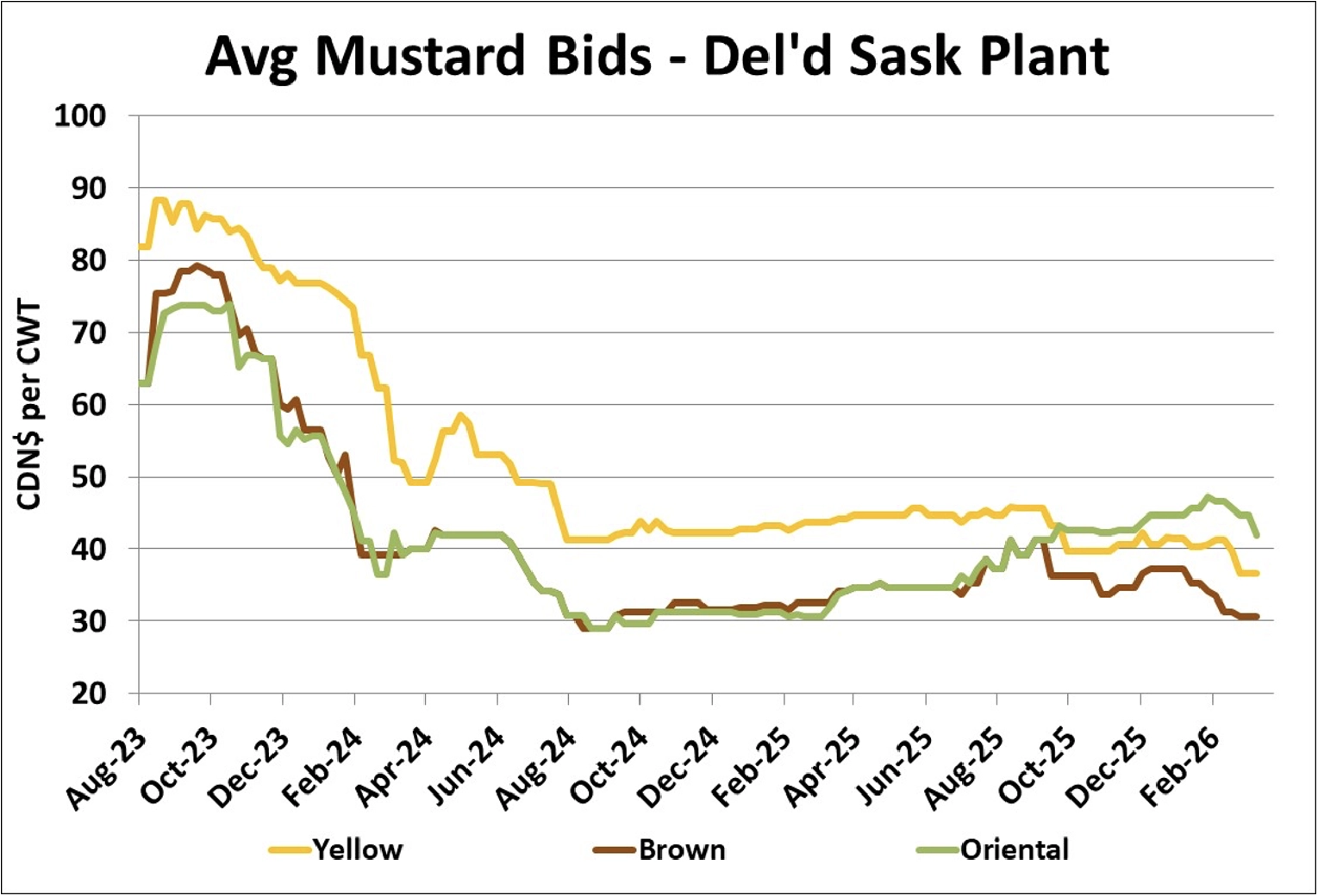

- Old-crop oriental mustard is continuing to decline from its peak in early February, which suggests that export demand has become quieter (or farmer selling has picked up or both). Old-crop yellow mustard bids have been gradually fading since early December while brown mustard bids remained flat in the last few months, although trade is less active. These weaker prices may be encouraging more farmer selling, which could add to the declines. New-crop bids are relatively steady, which suggests a more balanced outlook, although it’s still far too soon to draw conclusions.

Outlook

The lacklustre mustard exports are starting to exert a larger influence on mustard bids in western Canada. Even though supplies of good-quality mustard aren’t excessive, the market is feeling heavier due to the quieter demand. More downside risk is possible if farmer selling picks up in response to the lower bids. The new-crop market is still steady as the 2026/27 outlook seems to be fairly well-balanced.

{kind=link}

{kind=link}

{kind=link}

{kind=link}