Market Developments

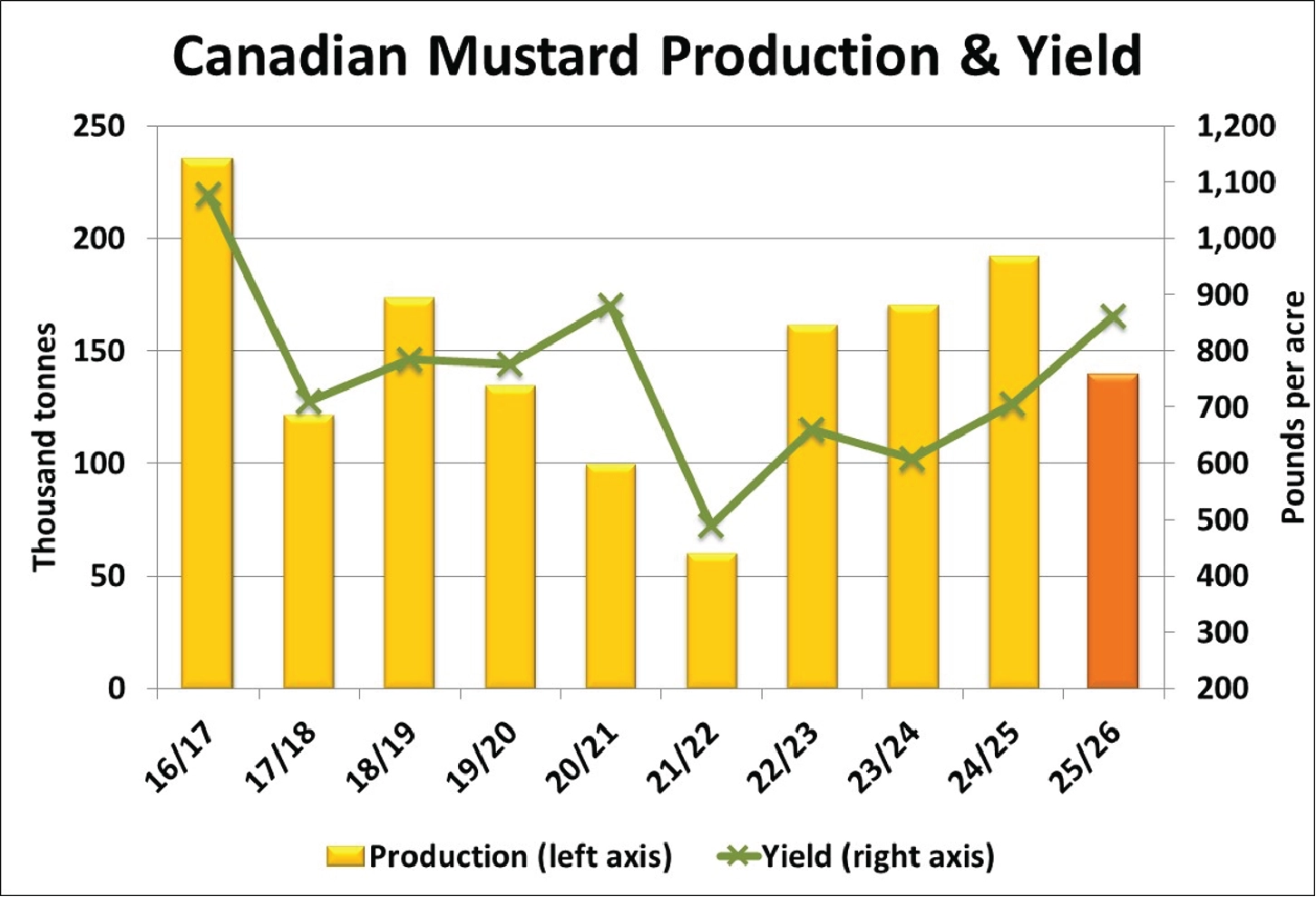

- The overall mustard production estimate from StatsCan of 140,000 tonnes was close to expectations. The 27% drop in the 2025 crop was the result of 40% fewer seeded acres offset by a yield of 862 pounds (17.2 bushels) per acre, 22% higher than last year.

- We have questions about StatsCan’s breakdown by type, which shows nearly flat yields for brown and oriental mustard and a sharp increase for yellow mustard. It’s especially noticeable that StatsCan’s yield for yellow mustard is higher than the other two classes, which doesn’t fit with historical performance. One other note; StatsCan showed oriental mustard with a smaller acreage decline than other classes, which could mean its production is overstated.

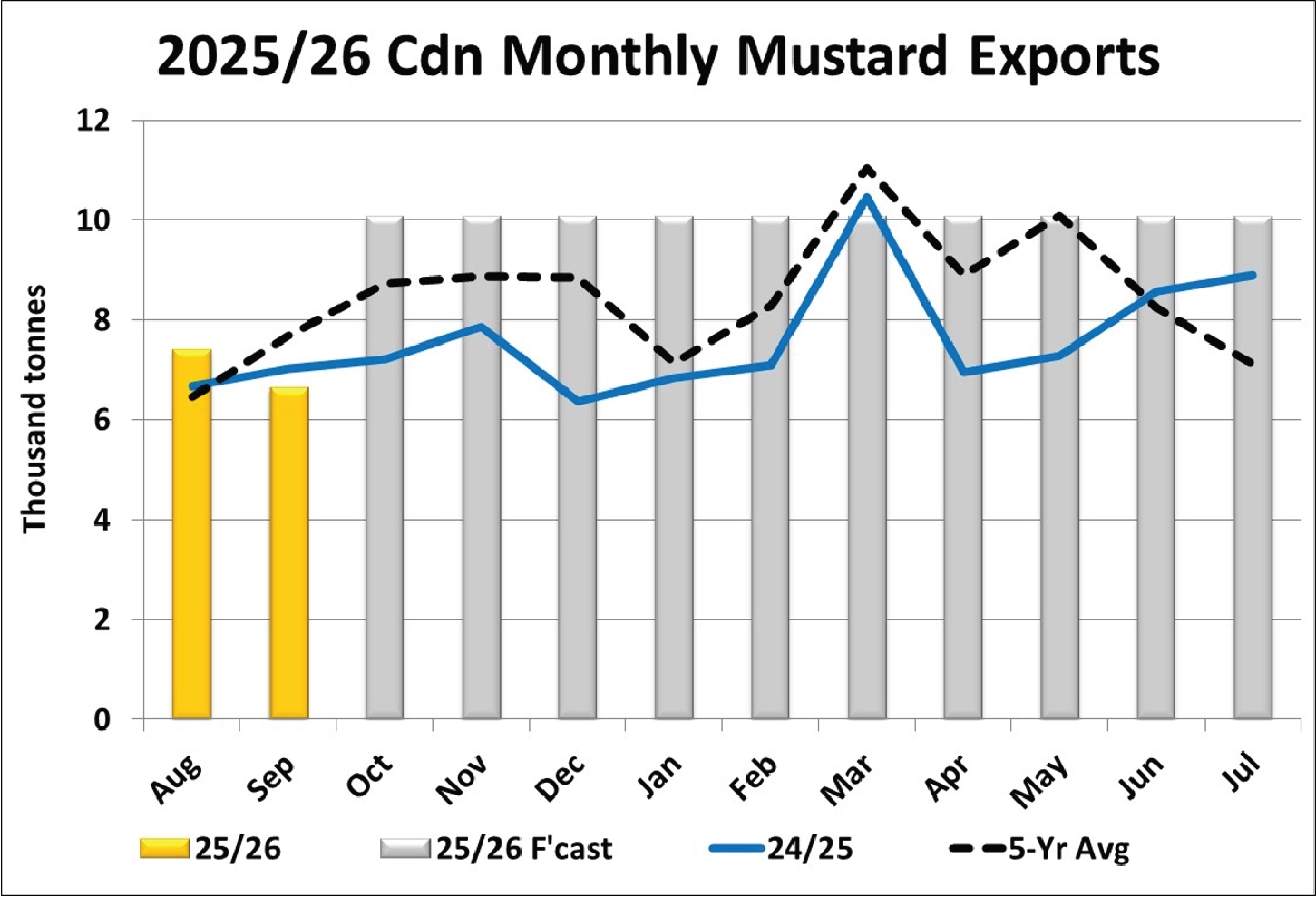

- It’s already fairly dated, but StatsCan’s latest trade data for September shows mustard exports of 6,600 tonnes, lower than a year ago and the 5-year average. Exports to the US were a modest 2,700 tonnes followed by Belgium at 2,300 tonnes. Our full-year forecast for 2025/26 is an aggressive 115,000 tonnes, partly due to expectations of larger exports to the US, but that will require a sharp increase in monthly volumes. It’s still too early to draw any real conclusions but volumes to Asia are up slightly from previous years, which could help explain the relative strength in oriental mustard bids.

- Mustard imports by the EU started the 2025/26 marketing year on a strong note but volumes have slipped in recent months, with 6,100 tonnes in October, the lowest total since May 2025. Imports from Canada dropped to 1,500 tonnes causing its market share to drop back to 25% after a couple of months of stronger performance. Ukraine was the largest origin at nearly 1,800 tonnes while imports from Russia dropped below 1,000 tonnes, the least since October 2024. Because of the larger volumes early in 2025/26, EU imports for the first four months reached 33,100 tonnes, ahead of last year at 26,900 tonnes and the strongest start since 2021/22.

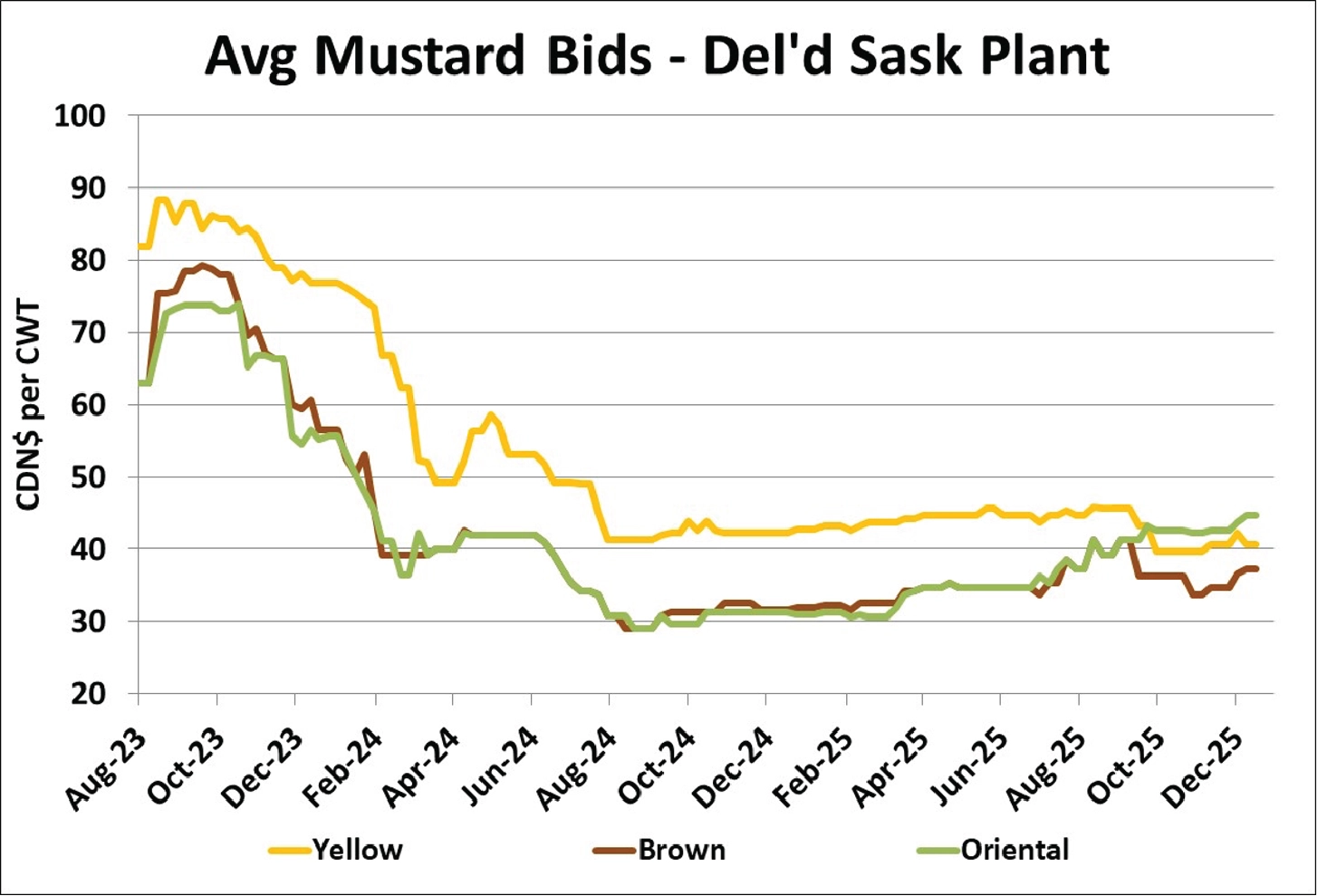

- While there has been some upward movement in some mustard bids since the harvest lows, particularly for oriental mustard, the overall market has been fairly steady this fall. As with most crops, the seasonal indexes tend to move higher from the harvest lows, with a fall peak occurring in Nov/Dec. For all three classes of mustard, the seasonal patterns tend to move sideways to slightly lower through the rest of the winter, more of a plateau than a peak. This suggests there’s limited potential for further upside this winter, although a small bump in early summer sometimes shows up for yellow and oriental mustard.

Outlook

Some bids moved higher shortly after harvest but since then, the mustard market has become quieter. On paper, supplies look comfortable but the lower quality of the 2025 crop means quantities available for Canadian processors and exporters aren’t as plentiful, which is providing some market support. Plus, as is often the case for mustard, farmers’ reluctance to sell is keeping the market firm. Even so, potential gains through the remainder of 2025/26 will be quite limited, especially if export demand remains subdued.

{kind=link}

{kind=link}

{kind=link}

{kind=link}