Market Developments

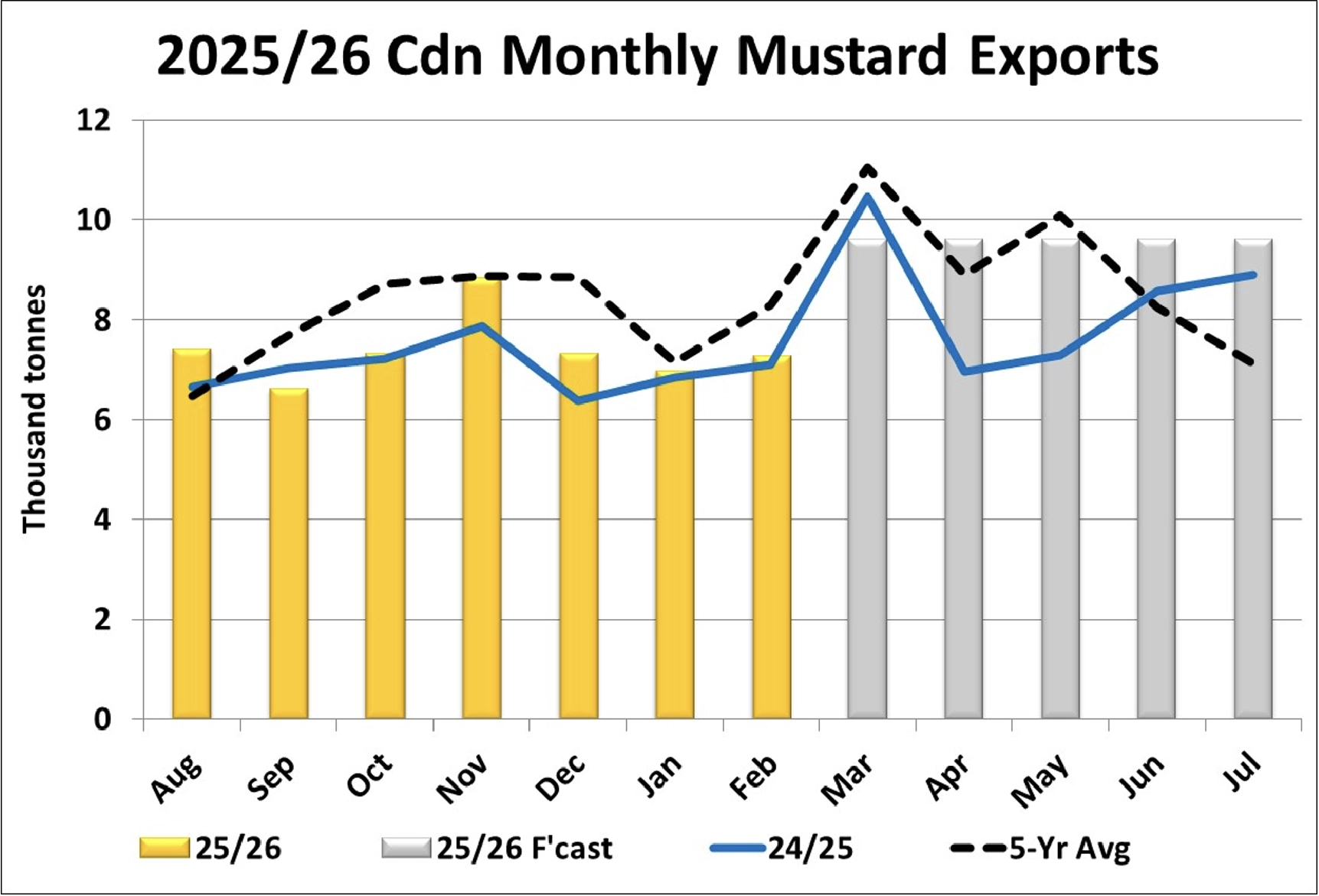

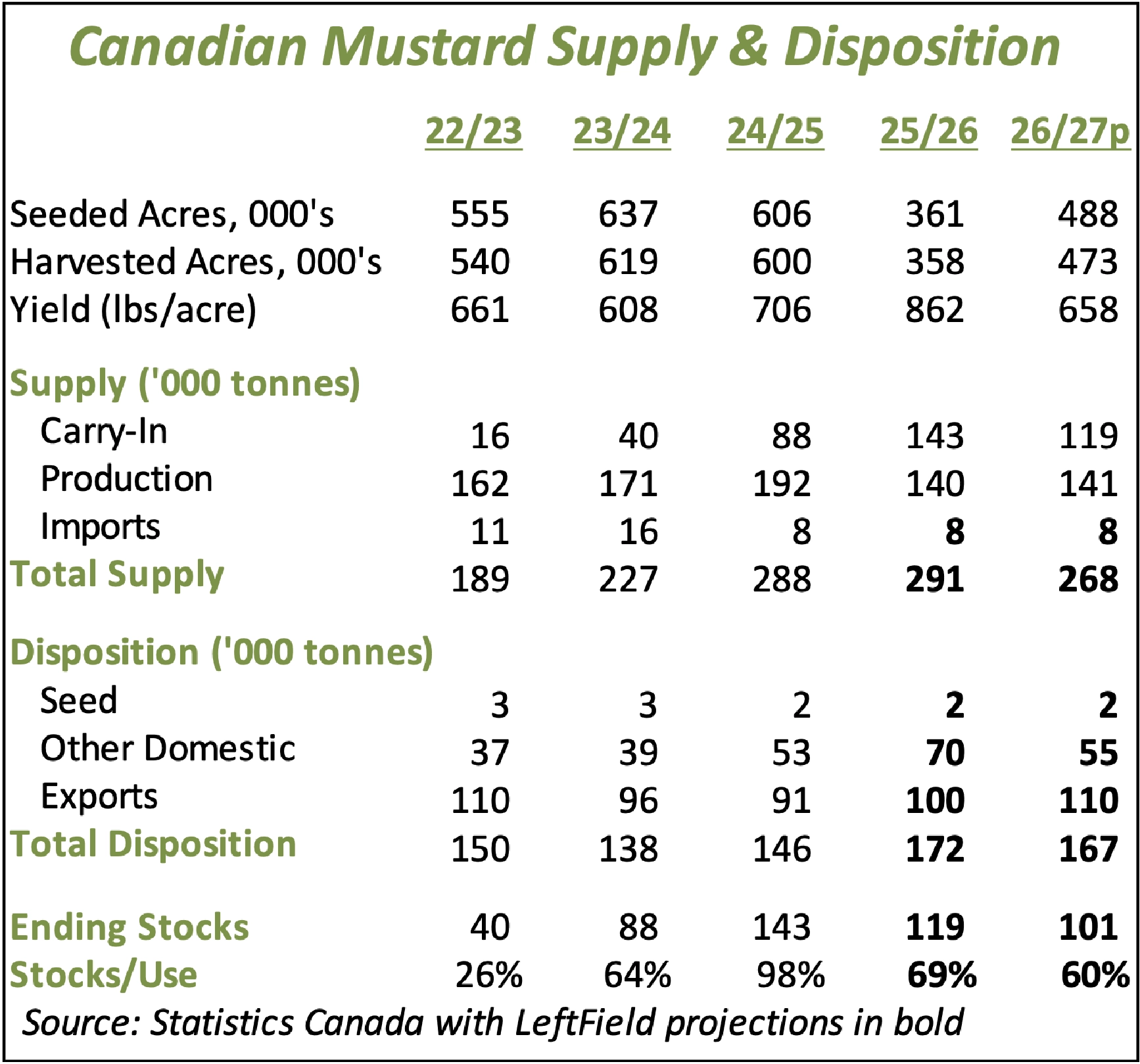

- Canadian mustard exports improved slightly in February to 7,300 tonnes, slightly ahead of last year but well below average. As usual, the US was the dominant destination, taking 4,600 tonnes of the total. Through the first seven months of 2025/26, exports totaled 51,900 tonnes, more than last year at 49,100 tonnes but less than the average of 56,000 tonnes. On average, volumes tend to pick up in March-May and a strong performance will be needed to reach our full-year export forecast of 100,000 tonnes (91,000 in 2024/25).

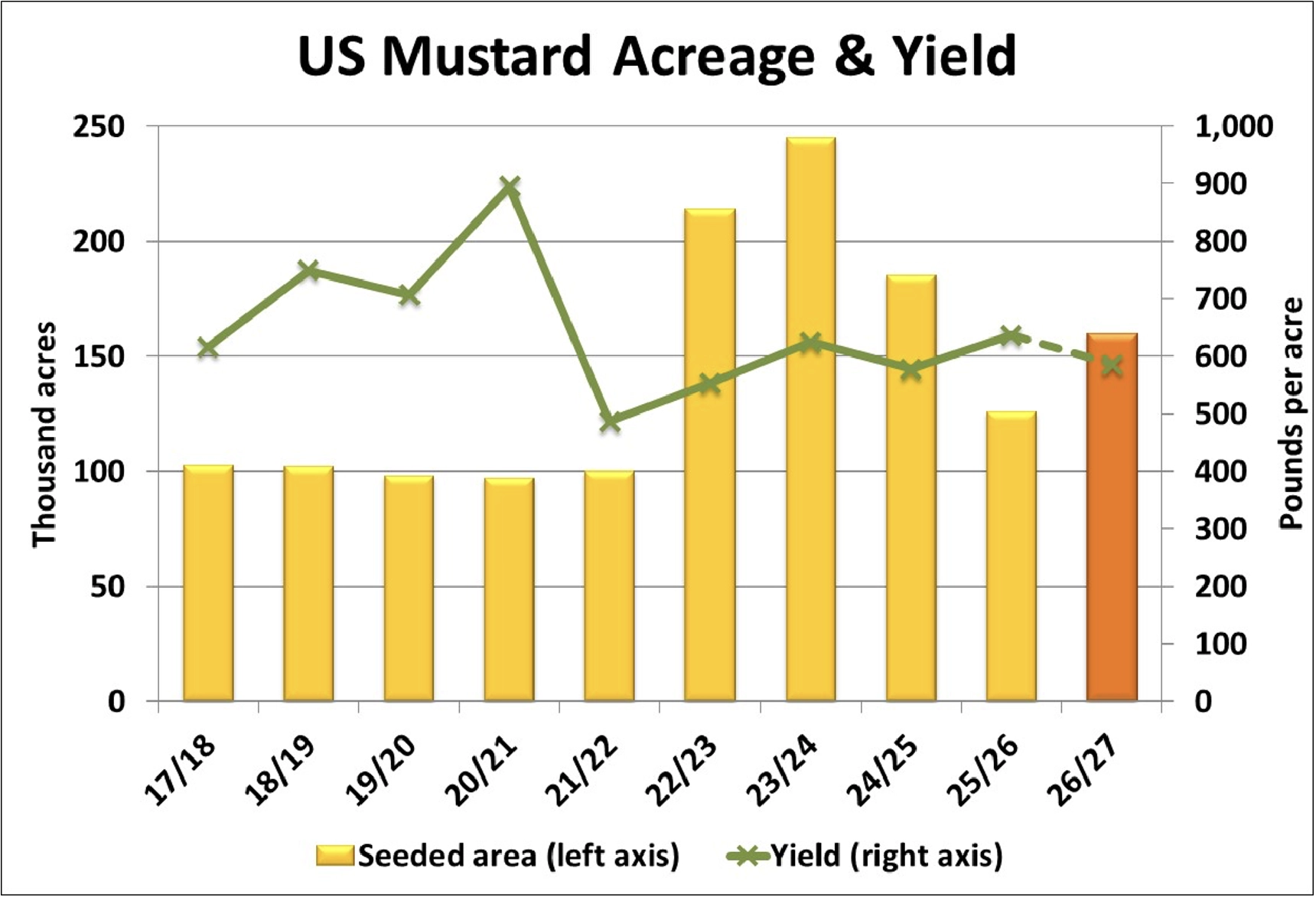

- The USDA doesn’t provide an estimate of mustard acreage in its Prospective Plantings report and the first real indication doesn’t show up until the FSA acreage declarations in August. For now, we’re looking at seeded area recovering slightly in 2026 to 160,000 acres. That would be a 27% increase from the low point in 2025, not far off the 35% increase in Canadian acreage. If we plug in the olympic average yield of 585 lb/acre, the 2026/27 US crop would come in at 86 mln pounds or 39,000 tonnes, 21% less than last year (which had higher than usual abandonment). Keep in mind, key mustard growing areas in the US are currently quite dry, similar to Canadian production regions.

- The yield reports from Saskatchewan Crop Insurance (SCIC) seem to confirm strong performance for mustard in 2025. The overall SCIC yield of 877 pounds (17.5 bushels) per acre is a bit higher than the StatsCan estimate of 847 lb/acre but almost identical with the Sask Ag yield estimate.

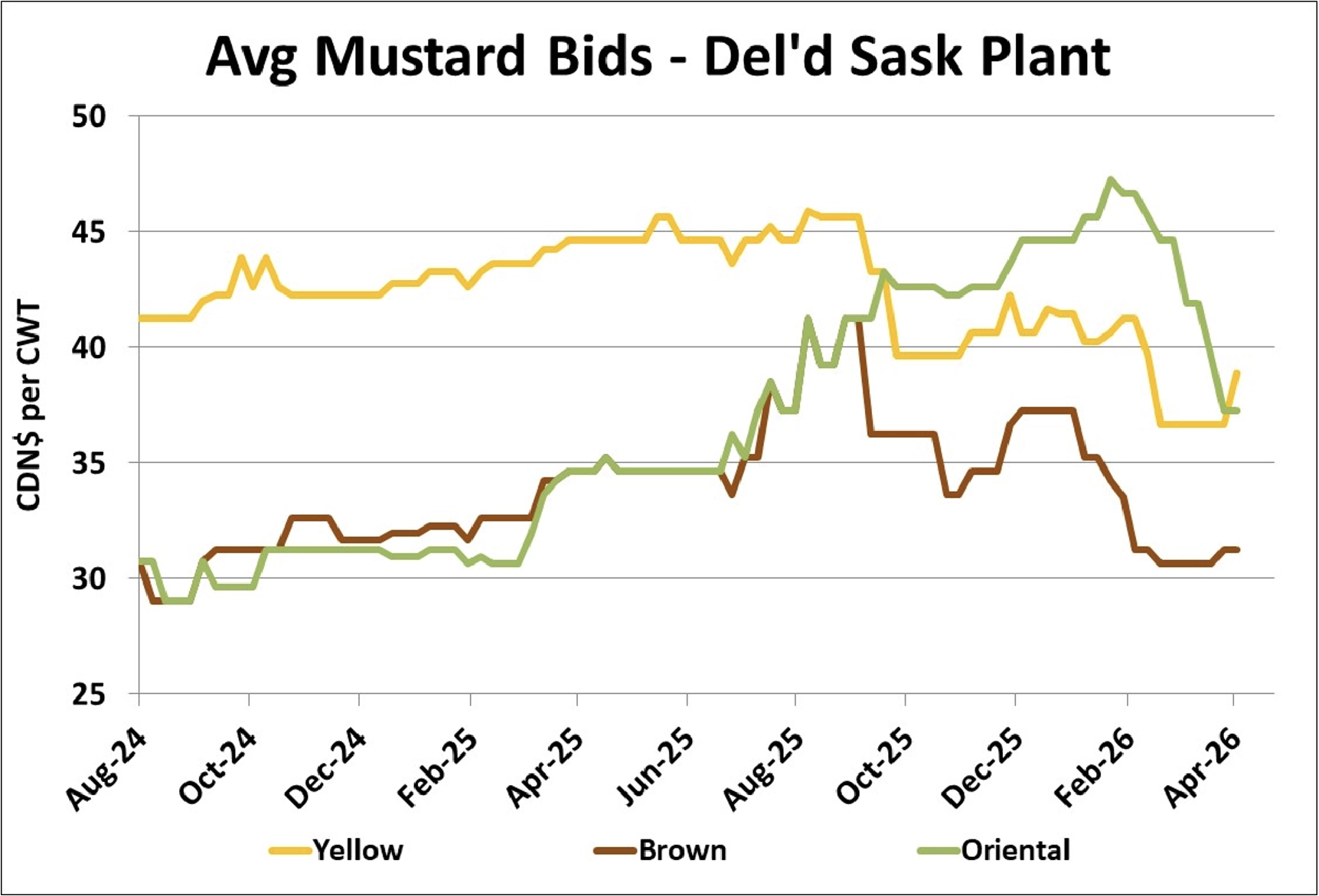

- The seasonal price indices for mustard generally move sideways through the first few months of the calendar year. The also don’t indicate there’s much opportunity for a late-season bounce in bids. At this time of year, the brown mustard price index is the weakest of the three and typically starts to go lower by the end of April, once the spring shipment through Thunder Bay is assembled. The oriental and yellow mustard indexes tend to remain steady until mid or late June before turning lower.

- The spreads between old-crop and new-crop bids are quite different by type. For yellow and brown mustard, new-crop bids are higher than old-crop, which would suggest a limited drop in old-crop bids in summer. For oriental mustard though, new-crop bids are lower and a larger seasonal decline is possible.

Outlook

In recent weeks, yellow mustard bids have been stronger than other classes but market activity for all three types has been quiet, typical for this time of year. We would expect prices to drift mostly sideways in the short-term before turning lower seasonally. New-crop bids are reflecting stronger buyer interest in attracting yellow and brown mustard acres while farmers’ intentions to plant more oriental mustard have caused those new-crop bids to weaken. In 2026/27, the more typical spread between the classes, with yellow on top, will likely resume.

{kind=link}

{kind=link}

{kind=link}

{kind=link}