Market Developments

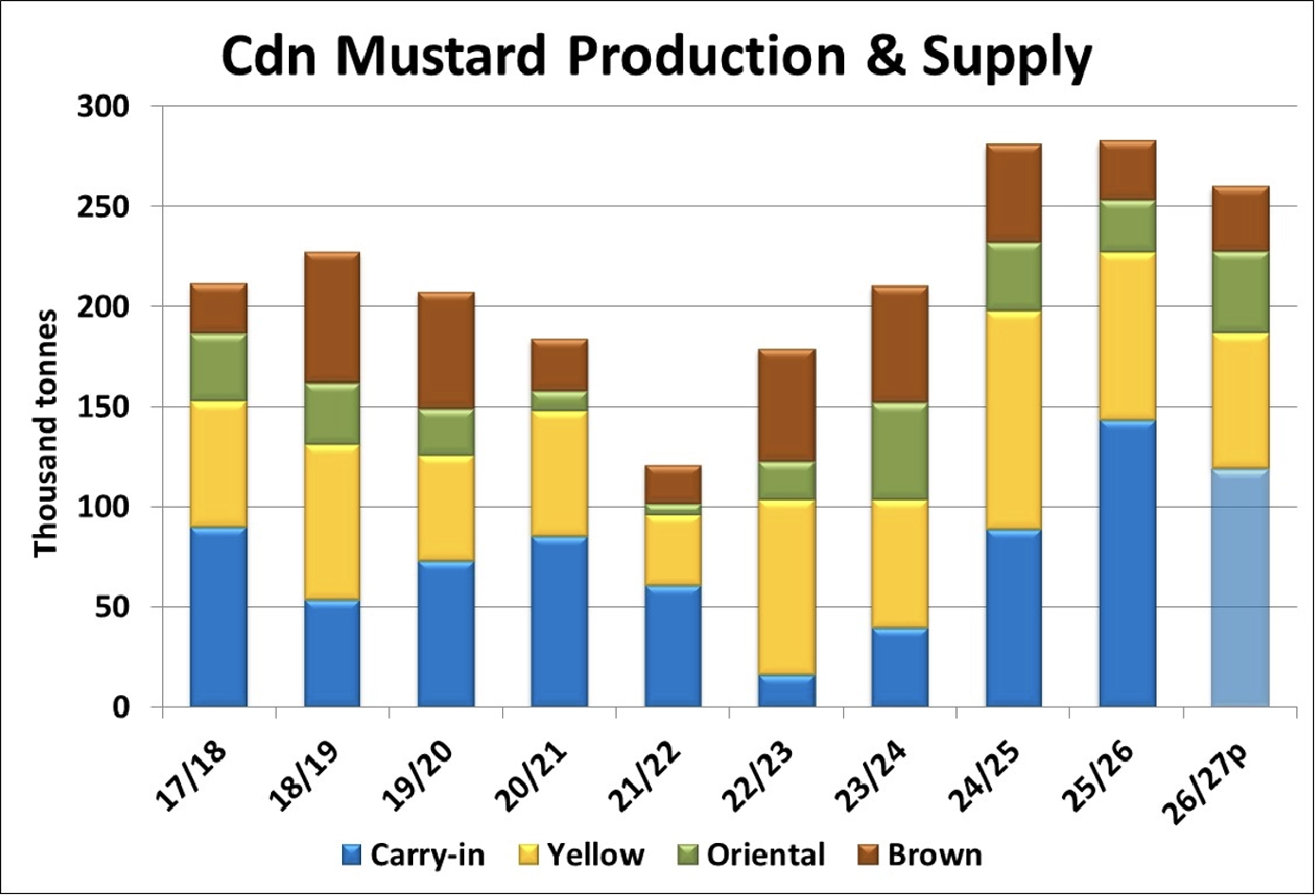

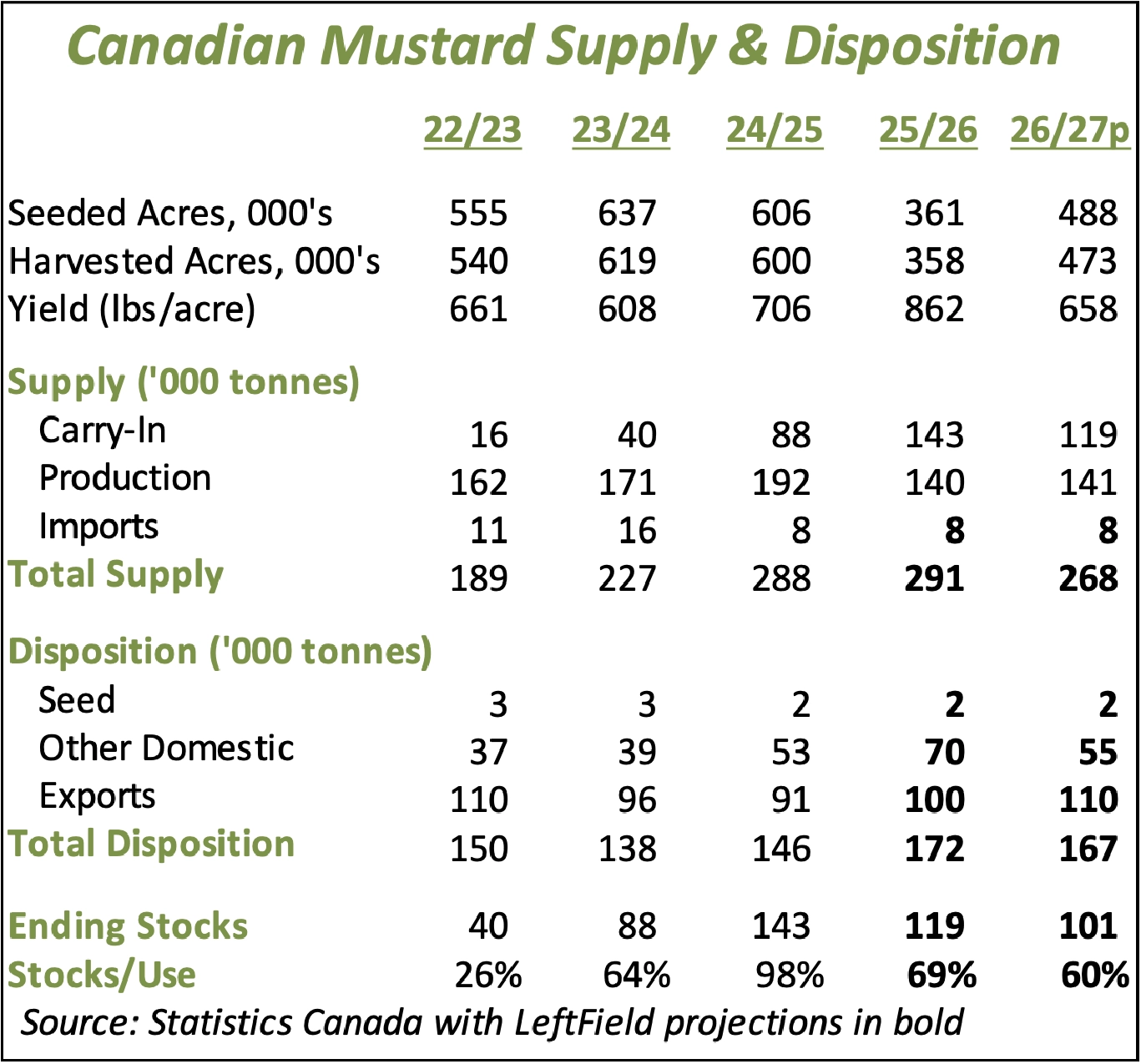

- Even with a 35% increase in 2026 mustard seeded area reported by StatsCan, there’s potential for next year’s mustard supplies to decline, especially for better quality mustard. We’re forecasting a smaller old-crop carryover from 2025/26, which would bring total 2026/27 supplies down to 268,000 tonnes, the lowest since 2023/24. Keep in mind, if we take out the 40-50,000 tonnes of 3Can or lower mustard in the carryover, 2026/26 supplies would be closer to 220-225,000 tonnes, which could actually start to feel “snug”.

- The mixed price performance in 2025/26 could mean acreage for various classes will respond differently. Stronger oriental prices (at least until recently) could result in a sharper rebound in seeded area, with smaller increases for yellow and brown mustard.

- Key mustard growing areas of SW Saskatchewan and southern Alberta are considerably drier this year than a year ago. Rainfall last August damaged crop quality in SW Saskatchewan but since then, precipitation in the region has been very low, with drought conditions intensifying. Keep in mind, the crop hasn’t even been planted yet and it’s far too early to make any serious yield forecasts, but favourable spring rains will be needed to get the crop off to a good start and regular precipitation throughout the season.

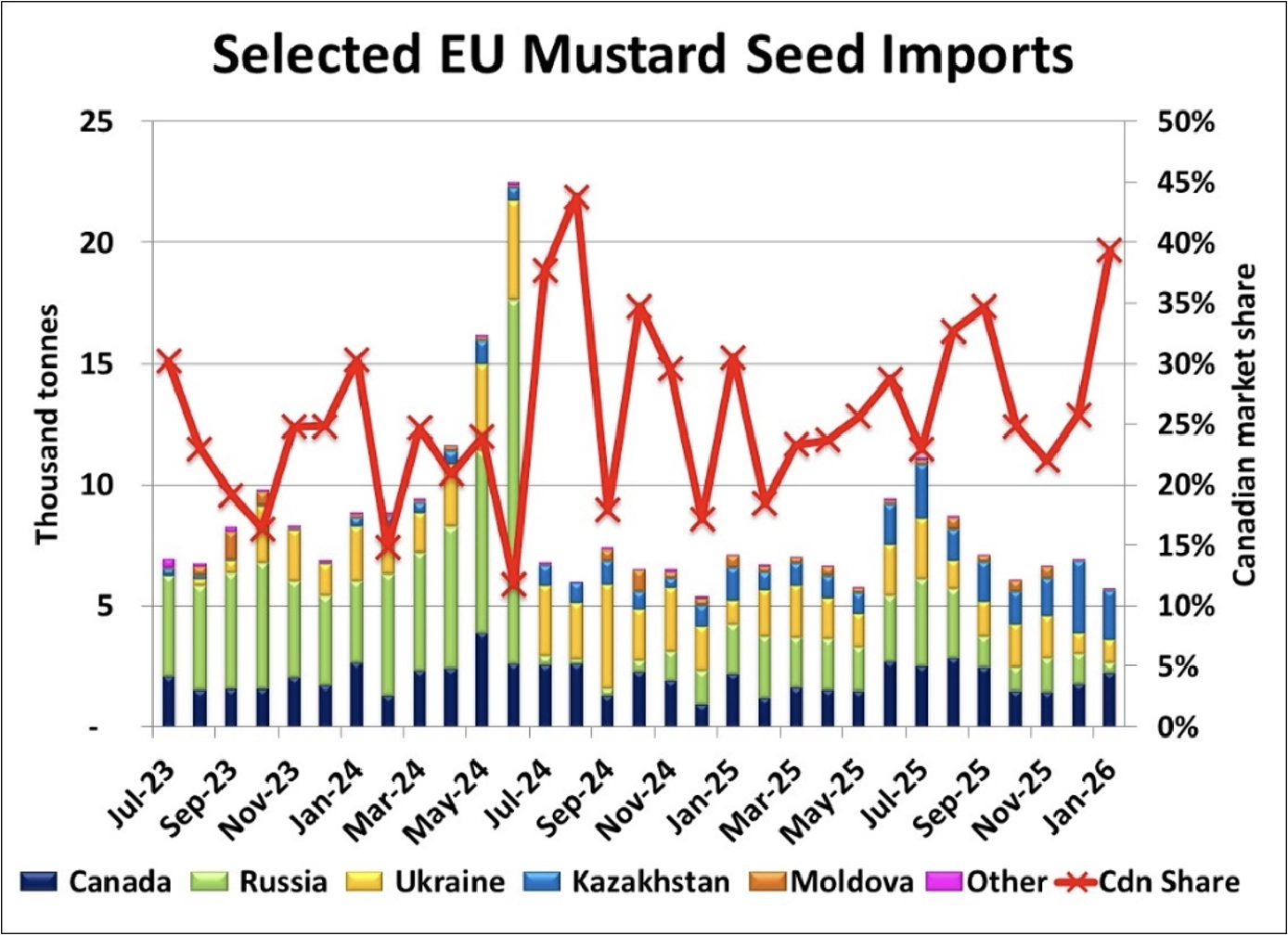

- Mustard imports by the EU dropped to 5,700 tonnes in January, the lowest total since December 2024. Meanwhile, imports from Canada at just under 2,300 tonnes were the most since September 2025. As a result, the Canadian share of the market rose to 39%, the most since August 2024. Through the first seven months of the EU marketing year, 52,500 tonnes were imported, ahead of last year at 46,100 tonnes and nearly on par with the 5-year average pace of 52,900 tonnes.

- After a strong start, Ukrainian mustard exports slowed recently, dropping below 1,000 tonnes in each of the last three months, with Europe still the main destination. With this slower pace, year-to-date exports are 11,100 tonnes, behind both 2024/25 and 2023/24. While we don’t have a firm estimate of Ukrainian mustard production in 2025, we expect the export pace is slipping due to limited supplies in the second half of the marketing year.

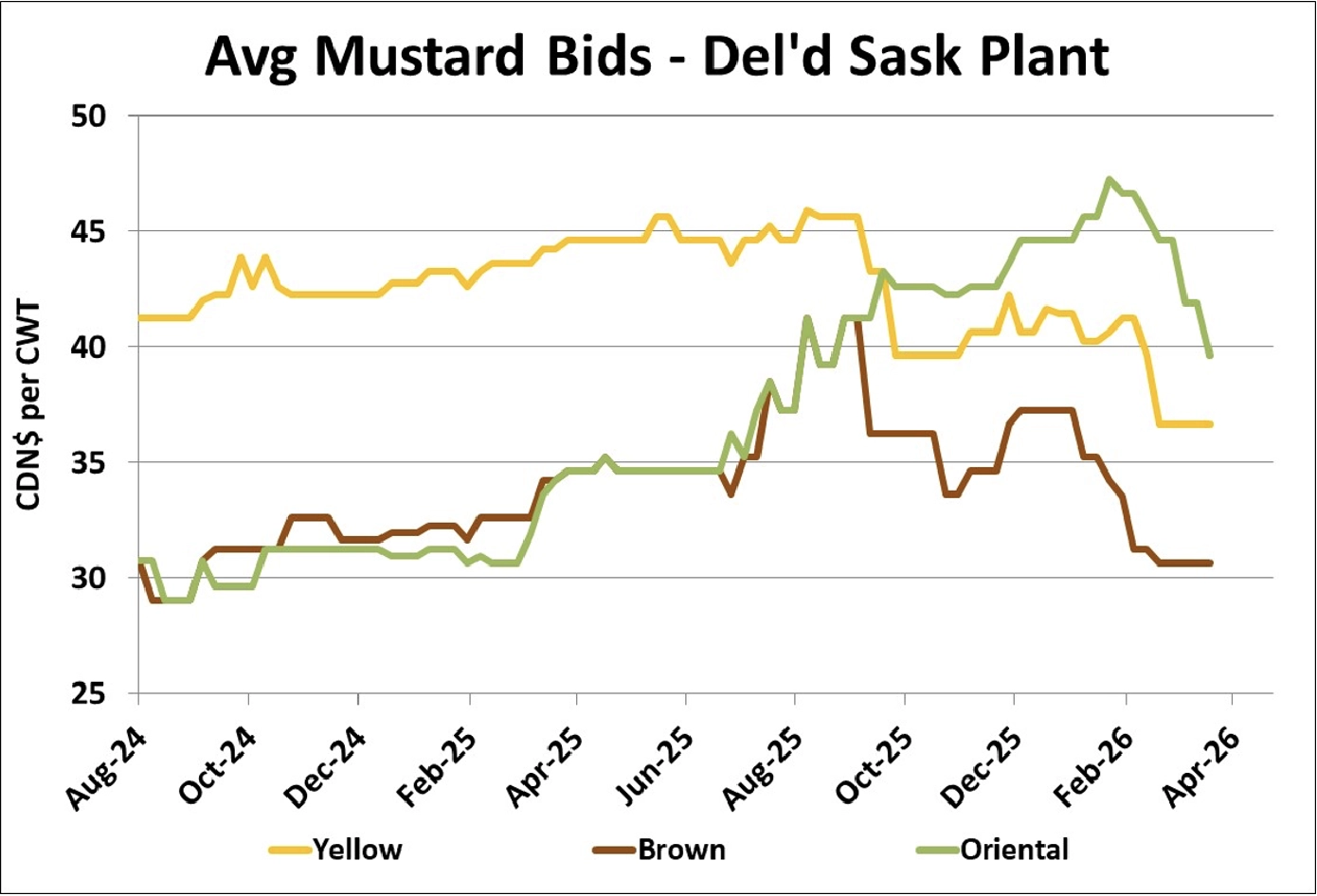

- Old-crop mustard bids are now settling into a lower range with only four months remaining in the 2025/26 marketing year. The drop in oriental mustard bids took longer to show up but that also means the recent declines have been steeper. Meanwhile, the weakness in yellow and brown mustard started earlier. There’s a good chance the low brown mustard prices have discouraged 2026 acreage, which is now causing new-crop bids to firm up. Meanwhile, seeded area of oriental and (to a lesser extent) yellow mustard will show larger increases, and that’s now starting to weigh on new-crop bids for those two classes.

Outlook

At this point in the marketing year, mustard buyers have little need to increase coverage and that’s allowing prices to drift lower and making old-crop bids scarce. That’s especially the case since export demand has been quiet this year. Although the old-crop market has little upside potential, the new-crop outlook is a bit vulnerable due to moisture concerns, although it’s far too soon to draw conclusions. Increased acreage will keep a lid on prices in 2026/27, as long as yields are close to average.

{kind=link}

{kind=link}

{kind=link}

{kind=link}