Market Developments

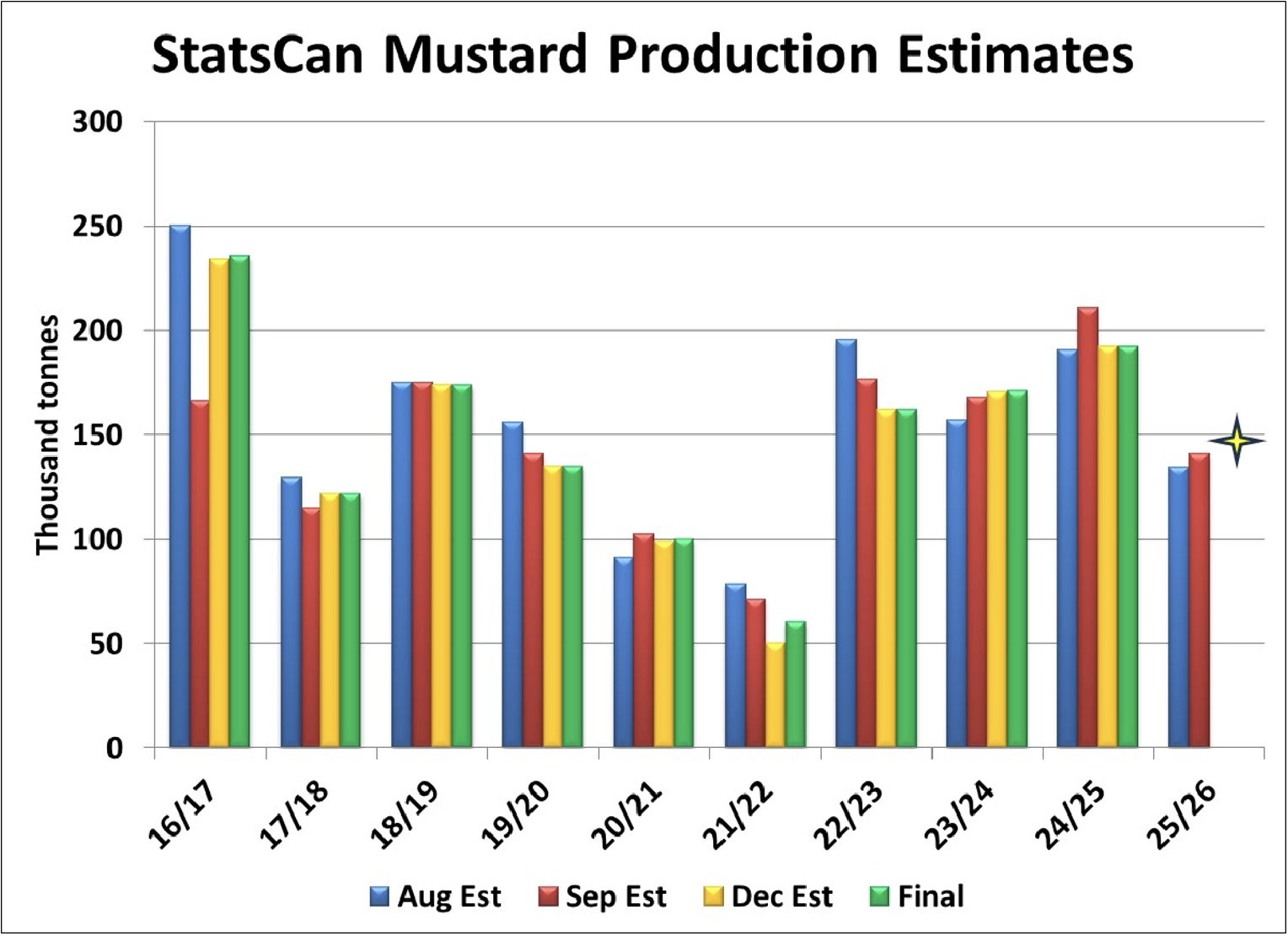

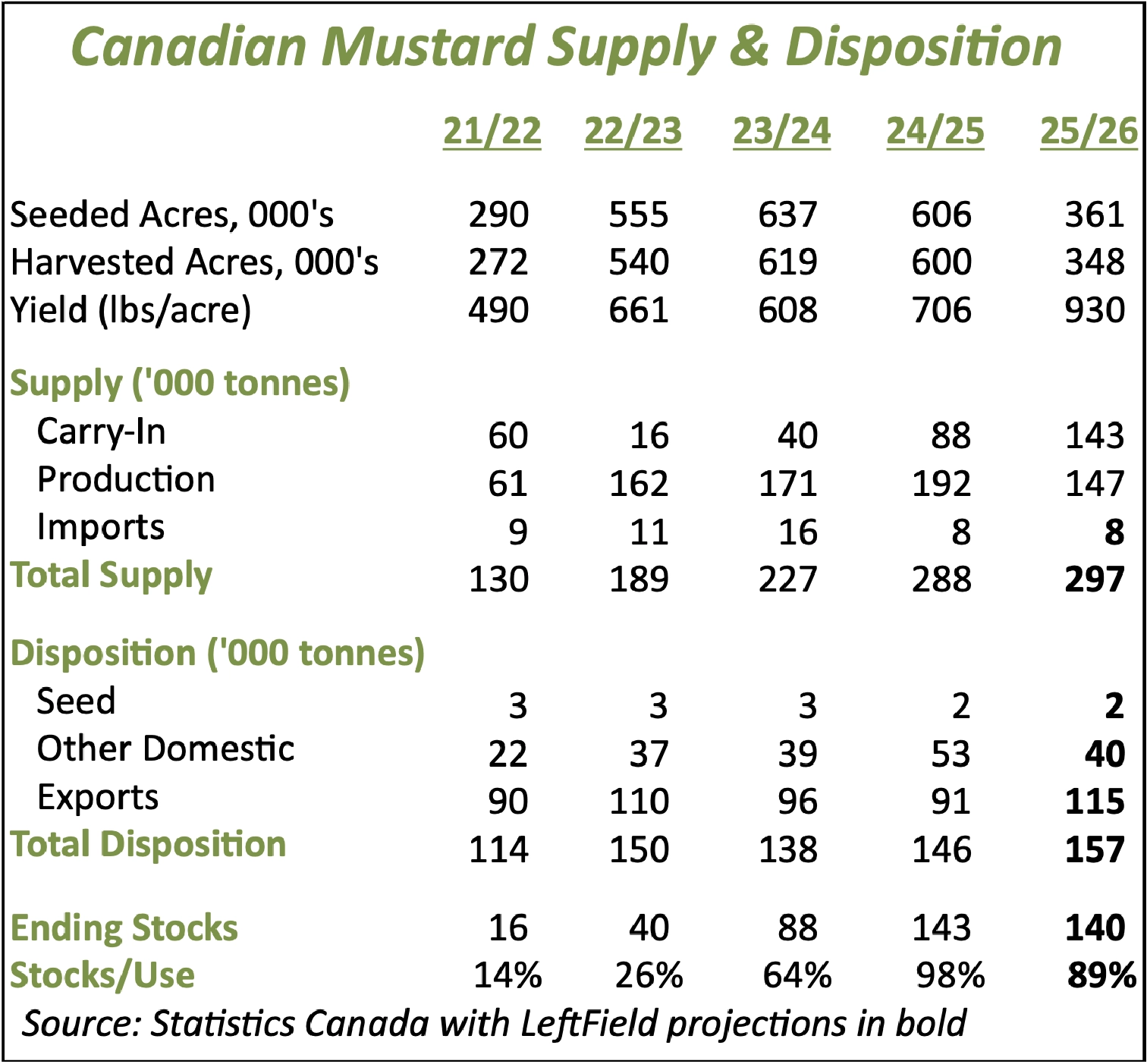

- This week’s mustard crop estimate from StatsCan may not move all that much from its September model-based number of 141,000 tonnes. This upcoming estimate is based on a farmer survey and could be slightly understated. Our last production estimate came in at 145-150,000 tonnes, 24% less than last year, due to a 40% drop in seeded area.

- The raw number of tonnes isn’t the full story though; the reduced crop quality in 2025 is a key factor in the supply picture. Based on Sask Ag’s quality breakdown, production of 1Can and 2Can mustard is 115-120,000 tonnes, 30% less than last year. And that’s on top of the poorer quality of the old-crop carryover from 2024/25.

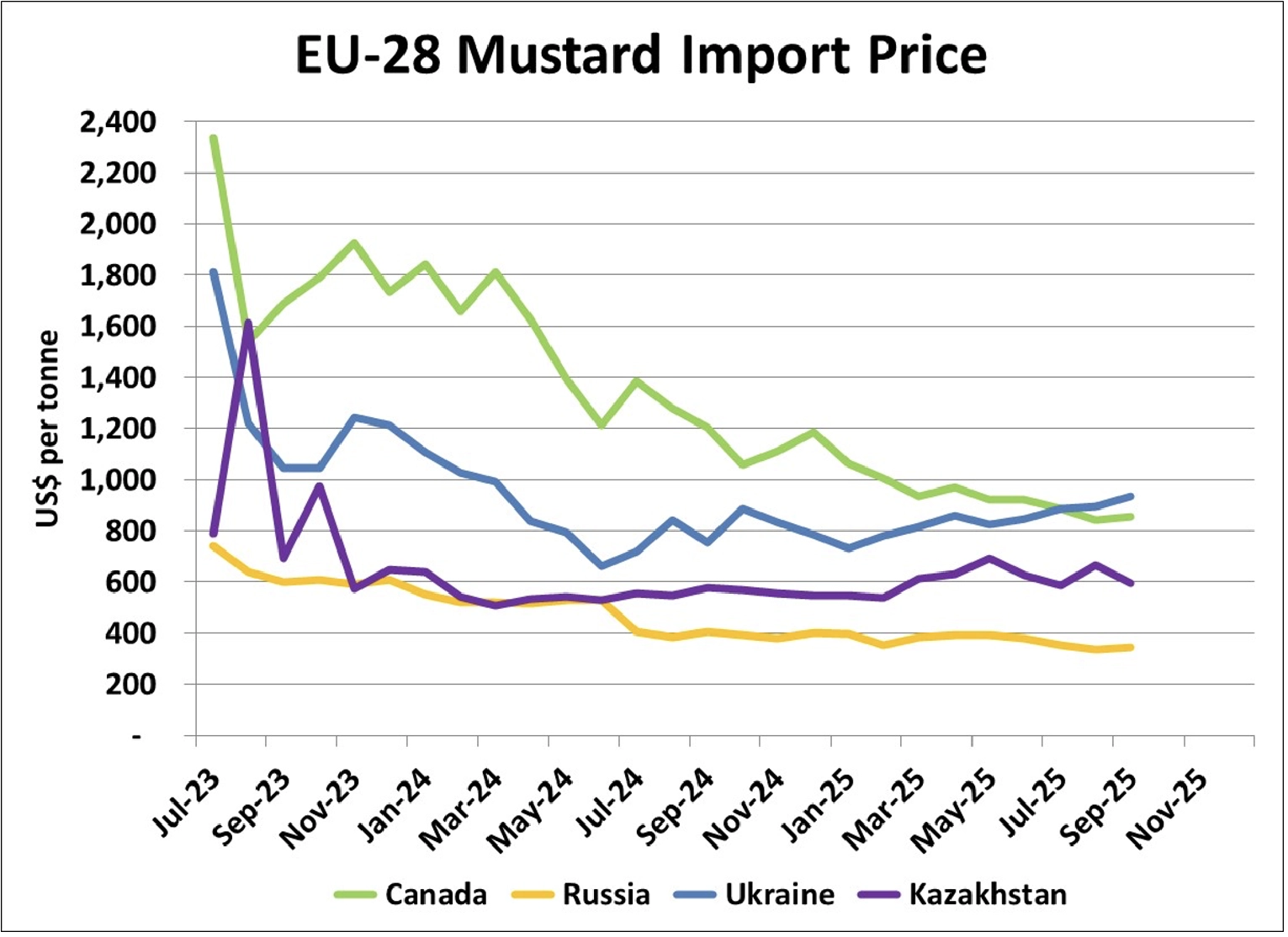

- Mustard imports by the EU declined to 6,900 tonnes in September, the lowest since May, but close to the average volumes seen over the last year. Canada remained the largest source again, with one third market share. Kazakhstan and Ukraine were the next two largest sources, with Russia accounting for less than 1,300 tonnes, the least since November 2024, when 50% import tariffs were about to be implemented.

- In the past few months, EU imports of Canadian mustard have picked up both in terms of tonnage and market share. That shouldn’t be a surprise, now that Canadian mustard prices have dropped enough to compete with mustard from other origins. In fact, if the uptrend in Ukrainian mustard prices is any indication, there could be a bit more upside possible for Canadian brown mustard. It’s also worth noting that despite 50% tariffs, Russian mustard continues to arrive in Europe, helped by large discounts. Currently, prices on Russian mustard are well below half of Canadian or Ukrainian mustard.

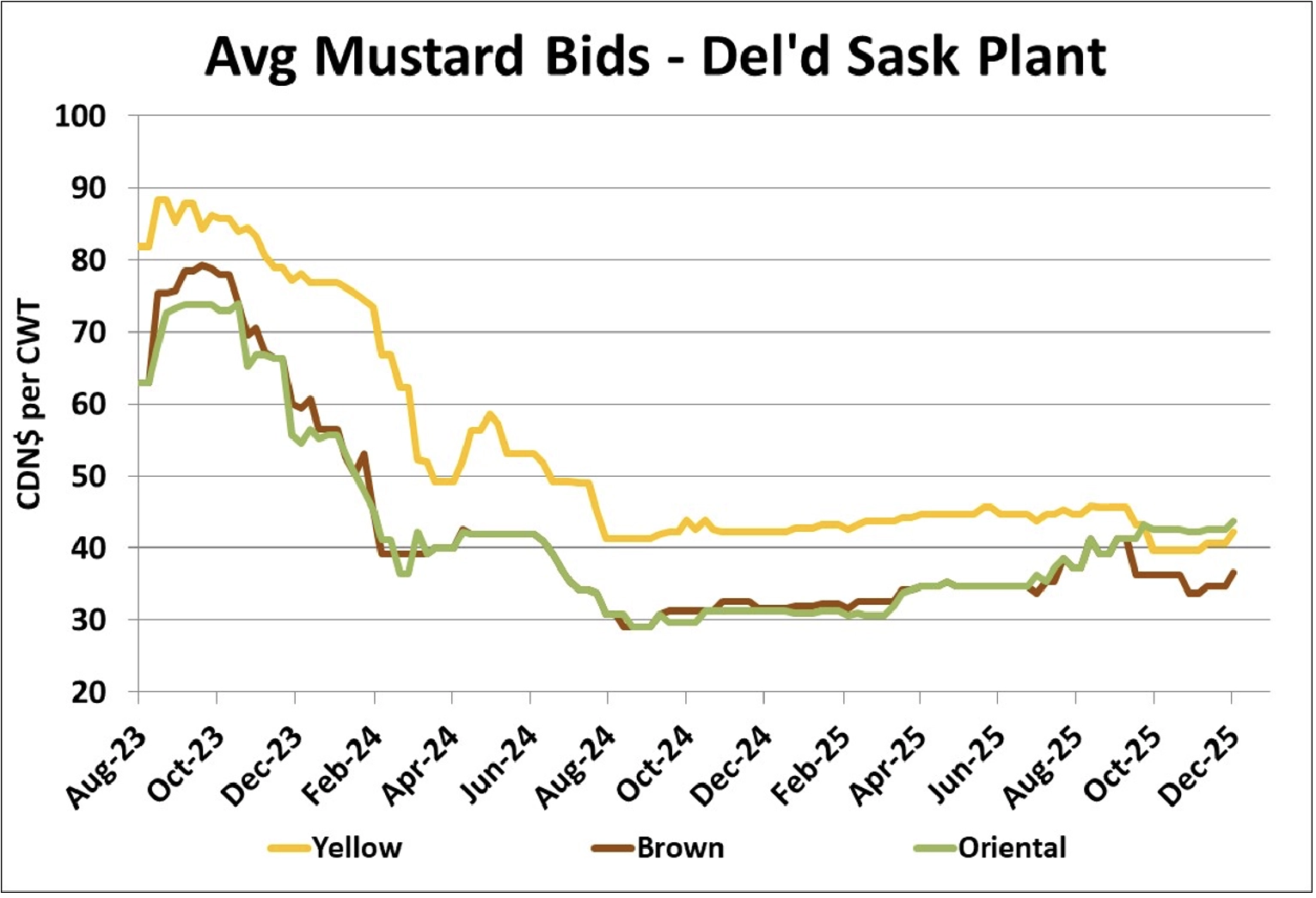

- There has been some movement in western Canadian mustard bids, although it’s still not all that noticeable. Yellow mustard mostly avoided the earlier seasonal weakness and continues to trend sideways. Oriental mustard has been moving higher since early 2025 and continues to strengthen, despite largely flat export trade. Brown mustard had also been trending higher until closer to harvest but then declined seasonally. In the last few weeks though, brown mustard bids have rebounded and are showing more strength too.

Outlook

Export business for all classes of mustard has not been “robust”, which suggests the price strength is driven less by demand and more by limited supplies of good quality mustard. It also helps that farmers are patient holders of mustard and have higher price targets in mind. The EU has access to supplies from the Black Sea region which will tend to limit upside for brown mustard while a smaller US crop could mean more support for yellow later in 2025/26.

{kind=link}

{kind=link}

{kind=link}

{kind=link}