Market Developments

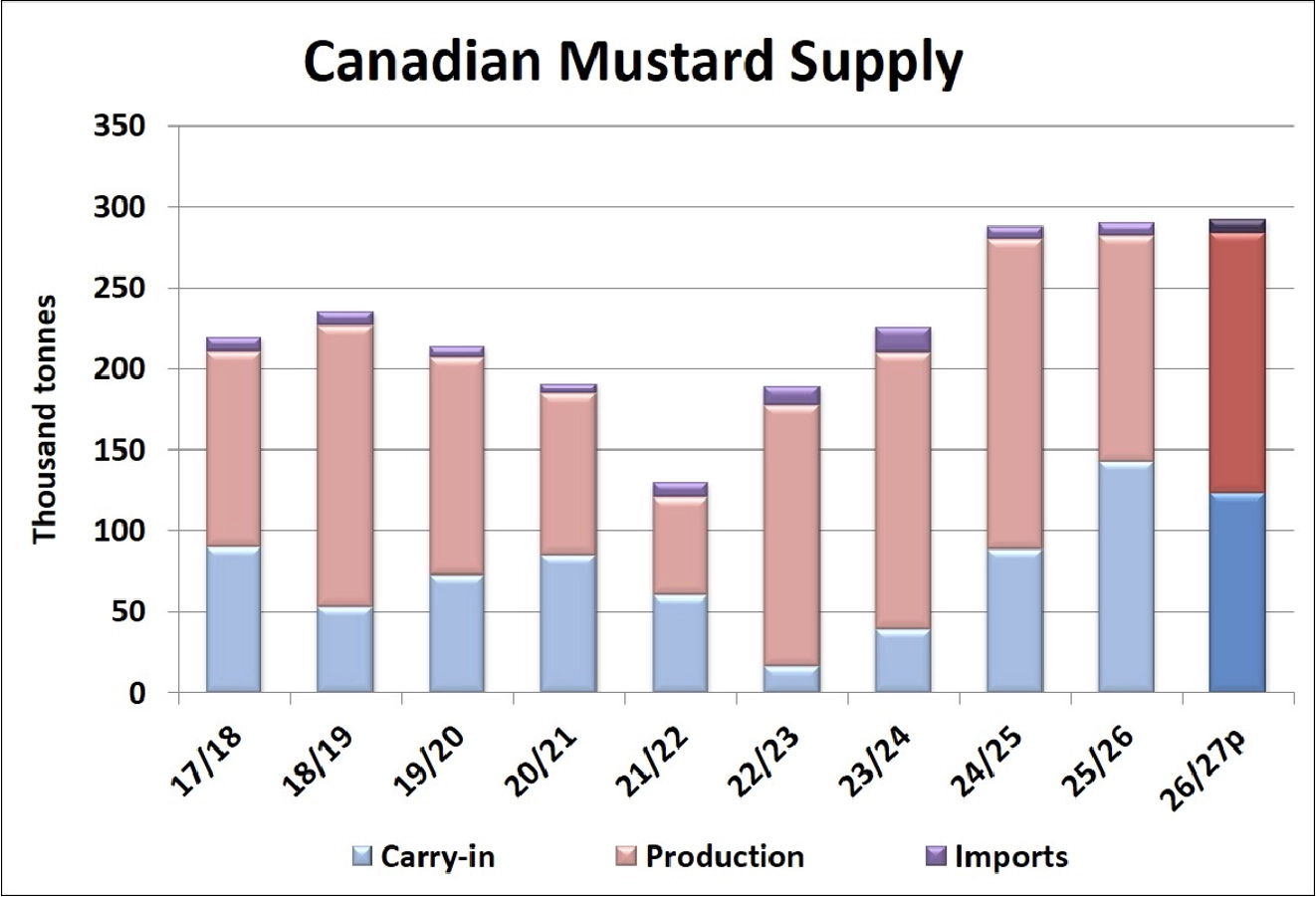

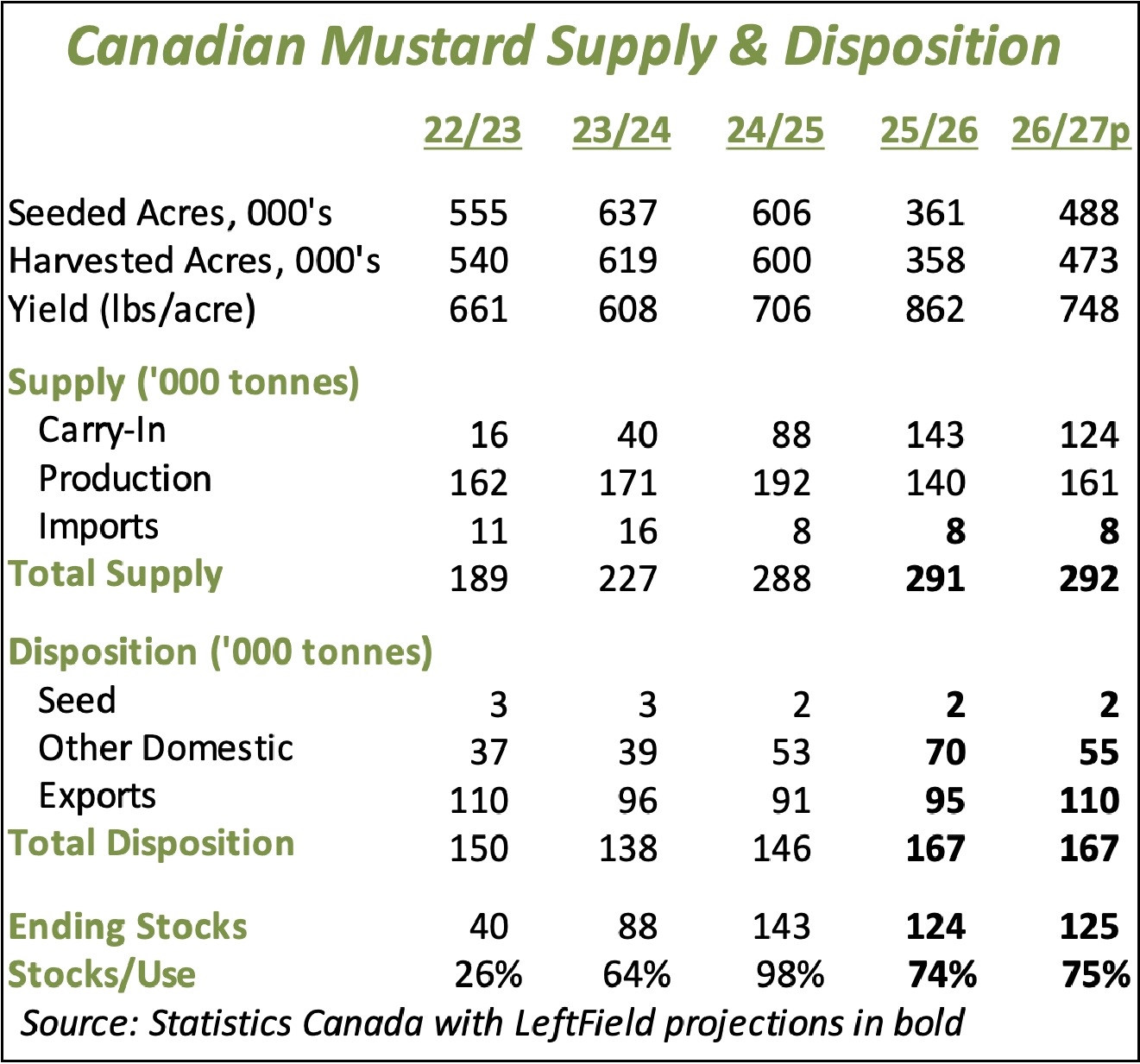

- Based on StatsCan’s 2026 estimate of mustard seeded area and a drop to the 10-year olympic average yield, production is forecast at 160,000 tonnes, up 15% from last year. That increase would be enough to offset the drop in old-crop carryover and keep 2026/27 supplies nearly unchanged at 290-295,000 tonnes. That said, a portion of the carryover is low quality mustard. Even so, it looks like there will be plenty of mustard available to meet export demand. For 2026/27, we have a bit more optimistic export forecast of 110,000 tonnes, although volumes have been subdued in the last two years.

- According to the last Sask Ag crop report, planting the 2026 mustard crop was still running at a very slow pace. As of May 18, 30% of acres had been planted, up from only 9% the previous week but still far below the 10-year average and the slowest start since 2014. Since that report date, southern Saskatchewan hasn’t received much moisture and a solid improvement was likely in the past week. Planting progress is much further advanced in Alberta, with 62% of mustard planted as of May 19.

- While there’s been lots of discussion about excess moisture and seeding delays, it’s important to note that the southern and western prairies didn’t get meaningful rains over the last few weeks. The soil moisture map shows a large portion of southern Saskatchewan is on the dry side. More importantly, the high temperatures are forecast to continue over the next few days will add to concerns about dryness. While the outcome is far from decided, the current weather outlook adds risk to the market.

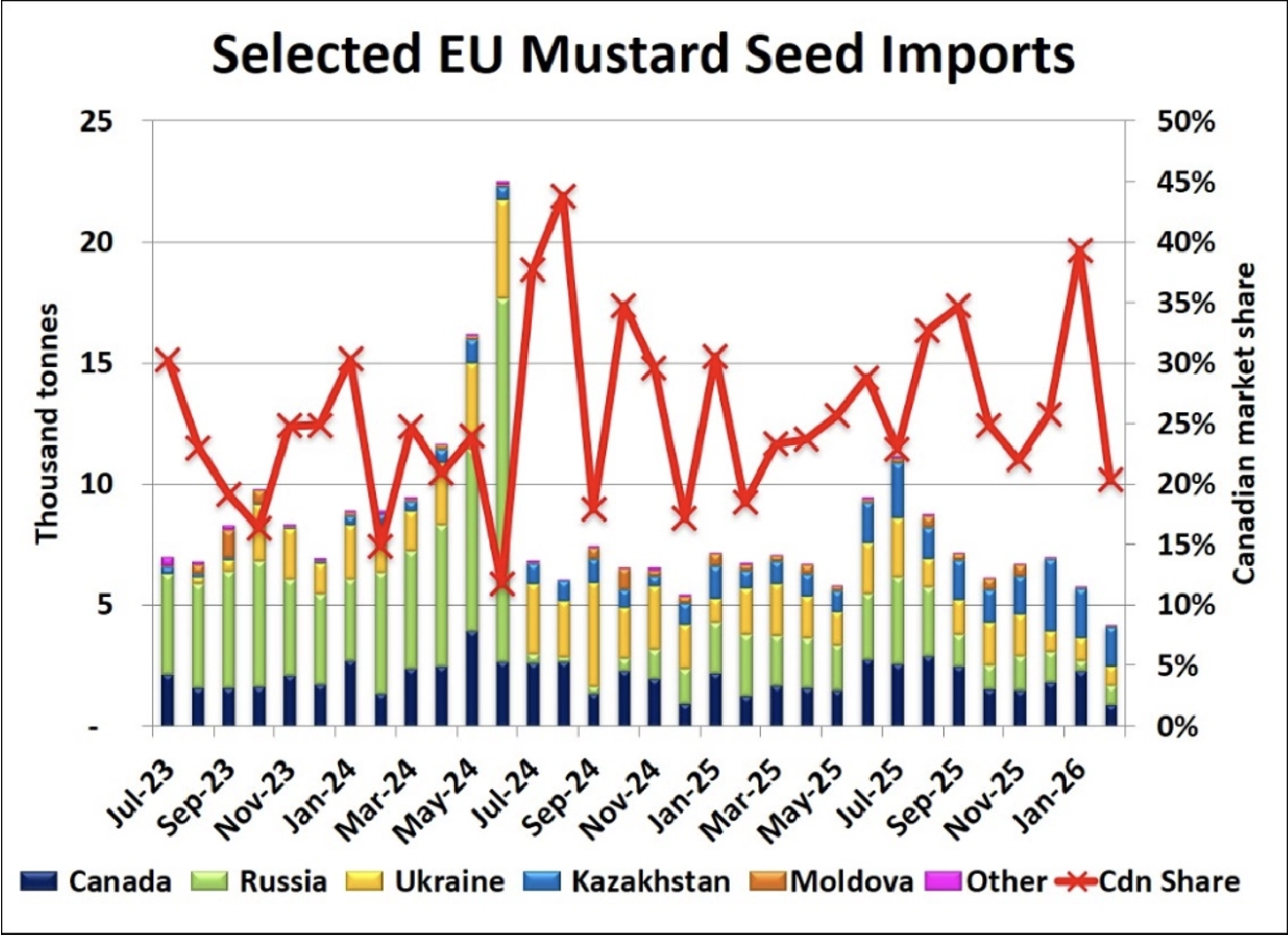

- Trade data from the EU is slow to be released but mustard imports for February aren’t very encouraging. The 4,100 tonnes for the month was the smallest total since June 2018 and the 840 tonnes from Canada were the lowest in our records going back to 2014. It’s also worth noting that Kazakhstan has become a significant source of mustard in 2025/26, despite its modest production last year.

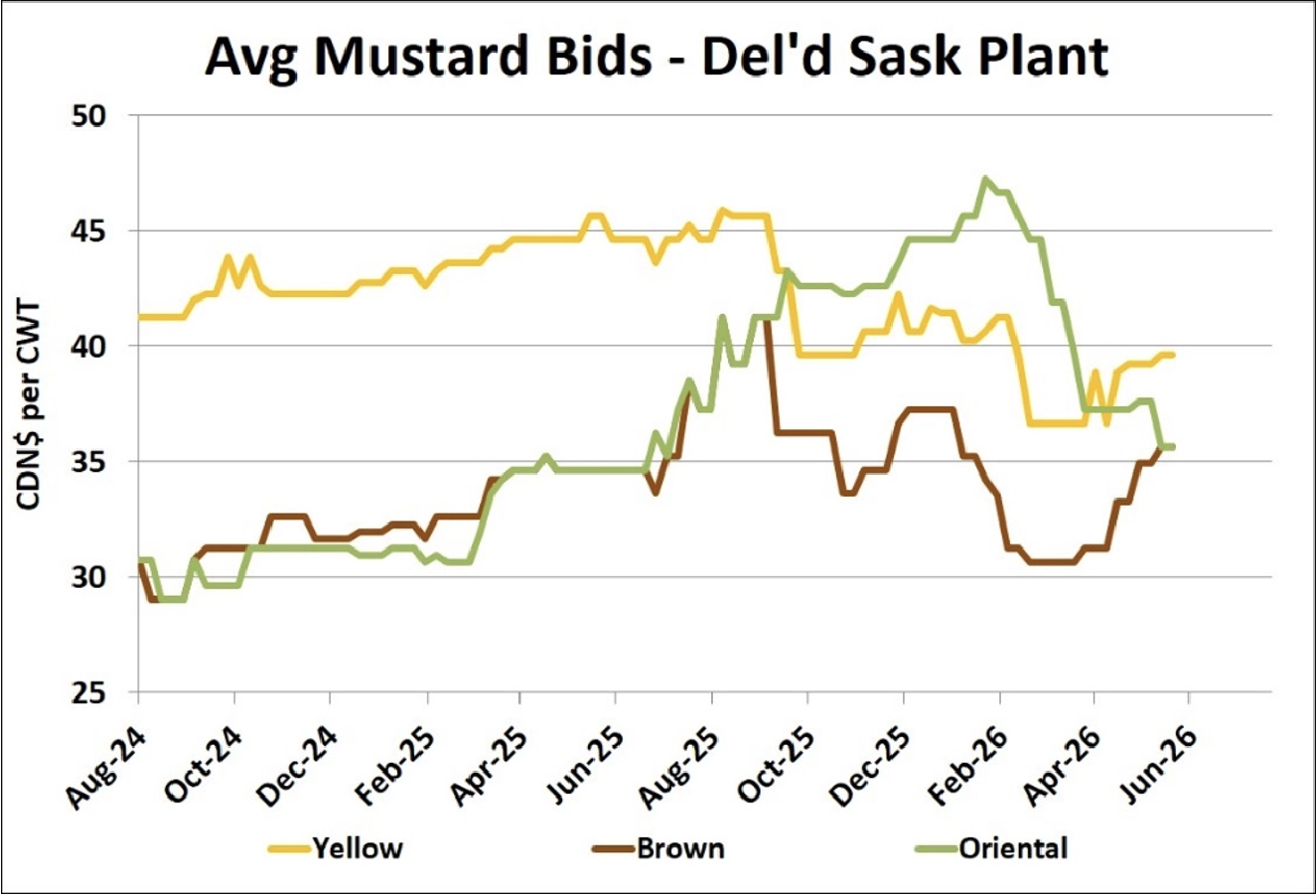

- The mustard market is fairly quiet at this time of year, allowing old-crop bids for yellow and oriental mustard to decline in line with seasonal tendencies. At the same time though, brown mustard has remained firm, an indication of relatively tighter supplies. For yellow and brown mustard, new-crop bids are well above the spot market, which signals some concern about seeded area in 2026. Meanwhile, new-crop bids for oriental mustard are slightly lower than the spot market, suggesting a more comfortable supply outlook, following the stronger performance earlier in 2025/26.

Outlook

The mustard supply outlook is quite different for the various types, with rising concerns about brown availability, while the outlook for oriental mustard is more comfortable. While the expected increase in seeded area should help maintain adequate supplies for 2026/27, if the hot dry conditions continue in the south, concerns will increase. At the very least, farmers will be less willing to sell, which would keep prices supported.

{kind=link}

{kind=link}

{kind=link}

{kind=link}